If you’re 55 with around $350,000 in super and seriously thinking about stepping back from work, you’re asking the right question at the right time. The honest answer is yes, retiring at 55 with $350K is possible, but the structure of how you do it matters more than the balance itself.

The challenge isn’t the number. It’s the timing. Super can’t be touched until 60. The Age Pension doesn’t start until 67. Retiring at 55 means you have a five-year gap before super access and a 12-year gap before Centrelink helps. That’s what the plan needs to solve, and it’s entirely solvable with the right approach.

What Is the Ideal Super Balance by Age in Australia?

Before working out whether $350K is enough at 55, it helps to know where it sits against the benchmarks.

The ideal super balance by age in Australia, according to ASFA modelling targeting a comfortable retirement at 67, looks roughly like this:

| Age | Ideal Super Balance (Single) | Ideal Super Balance (Couple) |

|---|---|---|

| 35 | $60,000 to $80,000 | $100,000 to $130,000 |

| 40 | $150,000 to $200,000 | $250,000 to $320,000 |

| 45 | $220,000 to $290,000 | $380,000 to $460,000 |

| 50 | $310,000 to $400,000 | $520,000 to $630,000 |

| 55 | $400,000 to $500,000 | $650,000 to $780,000 |

| 60 | $500,000 to $630,000 | $730,000+ |

At $350K, a single person at 55 is below the ideal benchmark by around $50,000 to $150,000. That sounds alarming, but benchmarks assume retiring at 65 to 67. If you’re planning to work part-time between 55 and 60, you can narrow that gap considerably before your super even gets touched.

For couples with $350K combined, you’re in tighter territory. For couples with $350K each, you’re actually close to benchmark. The per-person versus combined question matters enormously in this conversation.

The Three Phases of Retiring at 55 With $350K

Retiring at 55 in Australia plays out across three distinct phases, each with different rules and different income sources.

Phase 1 (Age 55 to 60): No super access. Your super stays locked away and continues to grow. All income during this phase must come from personal savings, investments outside super, property income, or part-time work. At 5 to 6% return, $350K grows to around $445,000 to $470,000 by the time you access it at 60, even without additional contributions. That five years of tax-advantaged compounding is one of the strongest arguments for leaving super untouched during this phase.

Phase 2 (Age 60 to 67): Super access, no Age Pension. At 60 you can access your super tax-free and convert it to an account-based pension. This is where $350K starts generating income. At 5% drawdown, that’s around $17,500 to $23,500 per year depending on how much your balance has grown.

Phase 3 (Age 67 onwards): Age Pension begins. This is where the retirement plan shifts significantly. The Age Pension at the full single rate is around $29,000 per year. Combined with whatever remains in super, total income improves considerably. Most people with $350K at 55 arrive at 67 eligible for a full or near-full pension.

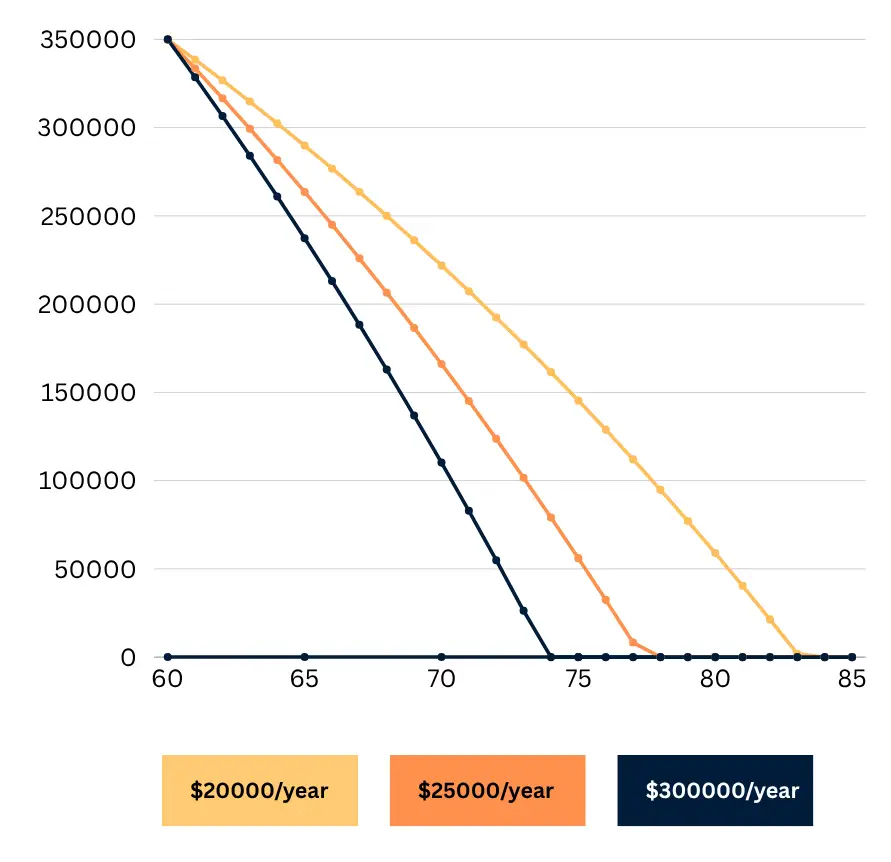

This Line Chart Showing how $350K depletes from ages 60 to 85 under spending levels of $20K, $25K, and $30K per year.

Ideal Super Balance at 55: Are You Behind, and Does It Matter?

One of the most common concerns people have at 55 is feeling behind on super. The benchmarks above suggest most people in their mid-50s should have $400,000 to $500,000 for a single comfortable retirement. At $350K you’re below that, but the gap is smaller than it feels.

Here’s why it matters less than you’d think for someone planning carefully:

The ideal super balance benchmarks assume no additional contributions between now and retirement. If you’re still working even part-time between 55 and 60, employer contributions at 12% of your income continue building your balance. Even $30,000 per year in part-time income adds $3,600 per year in contributions, plus whatever you choose to salary sacrifice on top.

The benchmarks also assume a traditional retirement at 65 to 67. If you’re willing to be flexible on spending in the early years and draw conservatively from super between 60 and 67, the gap between $350K and the ideal figure doesn’t have the retirement-ruining impact most people fear.

What matters more than hitting the ideal number exactly is having a clear plan for each phase.

Best Retirement Savings Account in Australia at 55: Where Your Money Should Be

This question comes up constantly for people in their 50s reviewing their financial position before retirement. The answer depends on whether you’re talking about super or money held outside super.

Inside super: For most Australians, super remains the best retirement savings structure available. Earnings in pension phase are tax-free, contributions get a tax concession, and the compounding over time is hard to beat on an after-tax basis. The ATO’s super page covers the contribution rules and tax treatment clearly.

Outside super (your bridge fund for ages 55 to 60): This needs to be accessible without penalty and structured for some stability. Options include high-interest savings accounts for liquidity, term deposits staggered annually to provide predictable income, a diversified ETF portfolio for income with some growth, and dividend-paying Australian shares for regular cash flow without locking up capital.

The main principle is to keep super untouched and growing during the 55 to 60 gap, and fund that period from outside assets. Every dollar that stays in super during those five years is working harder than it would anywhere else.

For guidance on working with a financial adviser to structure this properly, the MoneySmart working with a financial adviser page explains what to expect and how to choose the right person.

Over 55 Discounts in Australia: What You’re Entitled To From Day One

One of the most underutilised retirement planning tools is the range of concessions and discounts available to Australians over 55. These aren’t Age Pension entitlements. Many are available from your mid-50s onwards and can meaningfully reduce your living costs.

Commonwealth Seniors Health Card: Available to Australians of Age Pension age (67) who don’t receive the pension but meet the income test. Provides cheaper medicines under the PBS and access to some government concessions. Not available at 55, but worth planning for.

State-based seniors cards: Most Australian states offer a seniors card from age 60 (some from 65). These provide discounts on public transport, council rates in some councils, selected retail and service businesses, and various state government services. The exact benefits vary by state but add up considerably over a full retirement.

Private health insurance discounts: Some insurers offer loyalty discounts or reduced premiums for members over 55 or 60 who have maintained continuous cover. It’s worth reviewing your current policy and comparing options before you retire, as premiums become a significant budget item once employer group cover ends.

Travel discounts: Many Australian tourism operators, airlines, and accommodation providers offer senior and over-55 discounts. These aren’t available everywhere, but actively asking for them and using seniors card networks can reduce travel costs by 10% to 30% on domestic trips.

None of these replace income, but for someone with $350K and a modest spending plan, reducing annual living costs by even $2,000 to $3,000 through discounts and concessions adds meaningful longevity to the retirement plan.

How Long Will $350K Last if You Retire at 55?

At 5 to 6% investment return from age 60 (when super access begins), with the bridge years funded separately, here’s how $350K that’s grown to around $450,000 by age 60 tracks:

| Annual Spending from Super | Balance at Age 75 | Balance at Age 85 |

|---|---|---|

| $20,000 per year | ~$430,000 | ~$345,000 |

| $28,000 per year | ~$290,000 | ~$130,000 |

| $35,000 per year | ~$160,000 | Near depleted |

From age 67 the Age Pension adds around $29,000 per year for singles, meaning total income at the $28K drawdown scenario is around $57,000 per year from 67. That’s a solid, comfortable retirement for a homeowner.

Run your specific numbers through the free Wealthlab super calculator to see how your balance, spending, and timeline interact.

Funding the Gap: Ages 55 to 60

The five years between 55 and 60 are the most critical planning period for anyone retiring this early. Here’s what makes it work.

A dedicated outside-super bridge fund. As a rough guide, you need enough to cover five years of living expenses. At $30,000 per year, that’s $150,000. At $25,000, it’s $125,000. This doesn’t all need to be cash. A term deposit ladder (one maturing each year) combined with dividend income from shares is a practical and tax-efficient approach.

Part-time or flexible work. Even $15,000 to $20,000 per year in income cuts the bridge fund requirement almost in half. Many people at 55 aren’t done with work entirely. They’re done with full-time work. Consulting two days a week, seasonal work, or a small business venture can bridge the gap without depleting savings entirely.

Keep super invested in growth. The temptation to switch super to conservative or cash at 55 because retirement is approaching is a costly mistake. Your super at 55 doesn’t get touched for five years. It needs to keep working. Scott covered exactly why conservative doesn’t mean safe in Episode 1: Why Playing It Safe in Retirement Can Cost You More.

The ASFA Retirement Standard, which benchmarks what Australians actually need in retirement, is updated quarterly and available at superannuation.asn.au. It’s worth checking before you finalise your spending plan.

Healthcare Costs: The Budget Item Most People Miss

Healthcare is consistently one of the fastest-rising cost categories for retirees, and it’s the one most commonly underestimated in early retirement planning.

The Australian Institute of Health and Welfare tracks healthcare expenditure over time. Their data shows that healthcare costs rise steeply from the mid-60s onwards and are heaviest in the final years of life. For someone retiring at 55, building a buffer for healthcare that grows over time is more important than it looks in a spreadsheet today.

Practical steps include maintaining private health insurance continuously (the lifetime health cover loading applies if you take it out after 31 and let it lapse), budgeting for dental work as a separate line item rather than bundling it with general healthcare, and considering income protection insurance for the period before super access if you have any earned income. More detail on healthcare expenditure data is available from the AIHW health expenditure report.

FAQs

Can I retire at 55 with $350K in Australia?

Yes, with the right structure. You need savings outside super to fund ages 55 to 60, a clear plan for drawing from super between 60 and 67, and a realistic spending plan that keeps your balance working for the Age Pension top-up from 67. Home ownership is the key enabler. Renters need considerably more.

What is the ideal super balance by age in Australia?

ASFA benchmarks suggest around $400,000 to $500,000 for a single person at 55 to be on track for a comfortable retirement at 67. At $350K you’re below that, but part-time work and continued contributions between 55 and 60 can close much of the gap before you access your super.

What is the best retirement savings account in Australia?

Super remains the most tax-efficient retirement savings structure for most Australians, with tax-free earnings in pension phase and concessional tax treatment on contributions. Outside super, a combination of term deposits, ETFs, and dividend-paying shares provides a practical bridge fund for the years before super access at 60.

What discounts are available to over 55s in Australia?

State-based seniors cards are available in most states from age 60, providing public transport discounts, retail concessions, and reduced costs on some government services. From 67, the Pensioner Concession Card provides PBS medicine discounts and additional concessions for those on the Age Pension. Private health insurance loyalty discounts and travel concessions through seniors networks can also reduce living costs meaningfully.

How much outside super do I need to retire at 55 with $350K?

At $25,000 to $30,000 annual spending, you need around $125,000 to $150,000 outside super to fund the five years before access at 60. Part-time income can reduce this significantly. The bridge fund doesn’t all need to be cash. A mix of term deposits and investment income is more efficient.

How long will $350K last in retirement?

If your $350K grows to around $450,000 by the time you access it at 60, it can fund 20 to 30 years of retirement depending on spending levels and investment returns, particularly once the Age Pension supplements your income from 67.

Ready to Plan Your Retirement at 55?

Retiring at 55 with $350K isn’t about hitting a magic number. It’s about having a clear plan for each phase, from the bridge years through to the Age Pension at 67.

Book a free 15-minute call with Wealthlab to work through what your specific balance, spending plan, and timeline look like across all three phases.