If you are nearing 60 with $570,000 in super, you are in a stronger position than most Australians. $570K is close to ASFA’s comfortable retirement benchmark for singles and well above the median super balance for the 60 to 64 age bracket. The question is not really whether it is enough. It is how to structure it so it funds the lifestyle you want for 25 to 30 years.

Here is what the numbers actually look like.

Is $570K Enough to Retire at 60 in Australia?

Yes, for most single homeowners. $570K at 60 sits just below ASFA’s comfortable retirement benchmark of $630,000 for singles at age 67, but you are retiring seven years earlier, which changes the calculation.

The three things that matter most at this balance level:

Home ownership. Without rent or mortgage payments, your required income drops substantially. The ASFA comfortable lifestyle for a single homeowner costs $54,240 a year (February 2026). For a renter, the figure is considerably higher. $570K at 60 works well for homeowners; it is tighter for renters.

The seven-year gap. Your super access starts at 60, but the Age Pension does not start until 67. That gap needs to be fully self-funded. At $50,000 annual spending and 5% net returns, you would draw down roughly $220,000 to $240,000 between 60 and 67, arriving at pension age with around $330,000 to $350,000 remaining.

Staying invested. A balanced or growth investment option, typically 60 to 70% growth assets, keeps your money working over a 30-year retirement. Moving everything to cash at 60 risks losing ground to inflation year by year.

How Long Will $570K Last in Retirement?

Projection assuming 5% net annual return in an account-based pension:

| Annual spending | Super remaining at 67 | Years before balance runs low | With Age Pension top-up |

|---|---|---|---|

| $40,000 | ~$390,000 | ~26 years (to age 86) | Well into 90s |

| $50,000 | ~$340,000 | ~20 years (to age 80) | Mid to late 80s |

| $60,000 | ~$280,000 | ~15 years (to age 75) | Early to mid 80s |

| $70,000 | ~$210,000 | ~11 years (to age 71) | Late 70s to 80 |

The Age Pension changes the picture materially from your late 60s and 70s onwards. A single homeowner qualifies for the full Age Pension once assets fall below roughly $314,000, with a taper up to around $695,000. At $50,000 spending from 60, you would arrive at 67 with around $340,000, falling within the taper range and qualifying for a meaningful part pension.

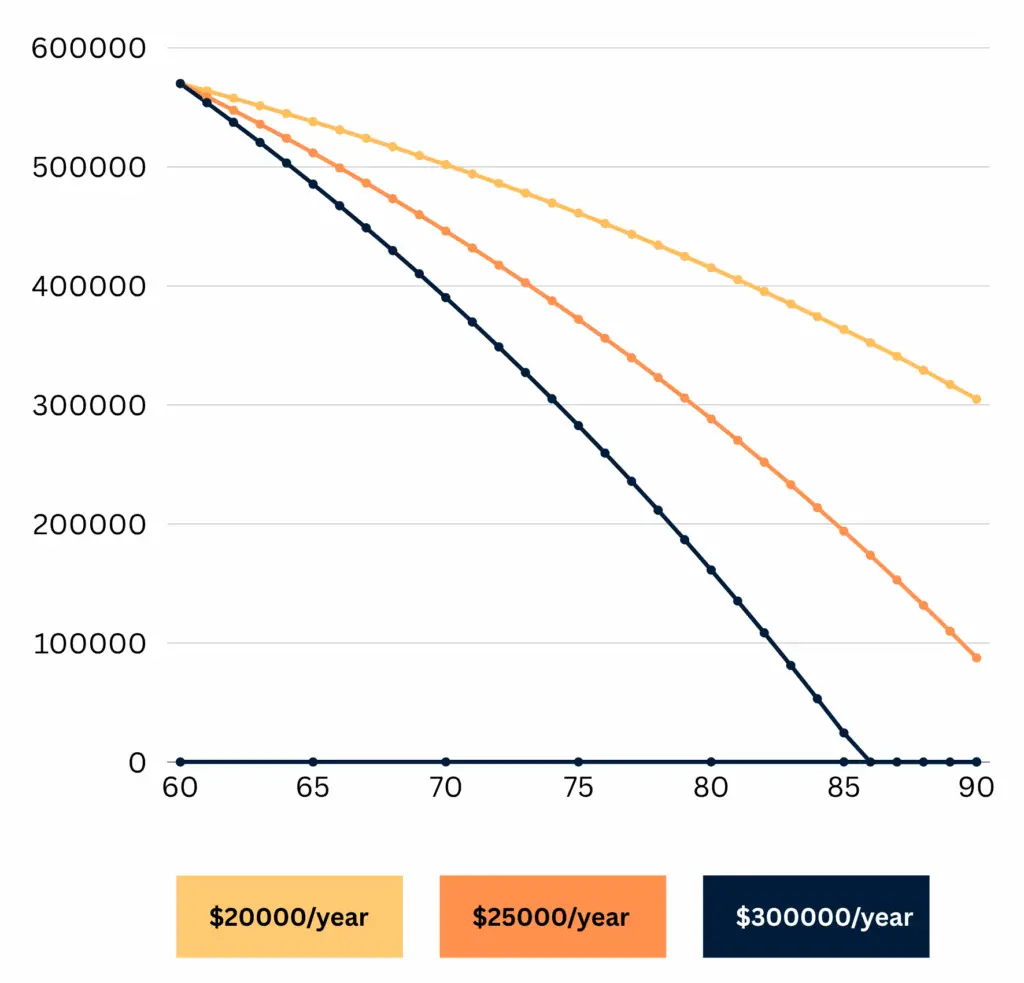

This Line Chart Tracks how $570K depletes from age 60 to 90 under annual spending levels of $20K, $25K, and $30K.

What Happens at Age 67?

Turning 67 is a key milestone in Australian retirement planning because that’s when you may become eligible for the Age Pension. This government support is designed to supplement your super, helping you maintain your lifestyle without over-relying on your savings.

- For singles, the Age Pension can provide around $28,500 per year.

- For couples, it can offer roughly $43,000 per year combined.

Receiving this income can significantly reduce the pressure on your super, meaning you won’t need to withdraw as much each year. For example, if your annual expenses are $30,000 and you receive $28,500 from the Age Pension, your super only needs to cover $1,500 dramatically extending the life of your $570K balance. This gives you more flexibility to manage lifestyle upgrades, unexpected costs, or small indulgences, such as travel, hobbies, or home improvements.

How Much Superannuation Do You Need to Retire at 60 in Australia?

This is one of the most-searched questions on this page and it deserves a direct answer.

ASFA’s benchmarks are set for people retiring at 67. Retiring at 60 requires more, because you are self-funding an extra seven years before the Age Pension arrives.

As a practical guide for homeowners:

- Modest lifestyle from 60 ($35,199 a year for singles): Around $350,000 to $450,000 at age 60 provides reasonable coverage to pension age.

- Comfortable lifestyle from 60 ($54,240 a year for singles): Around $650,000 to $850,000 at age 60, depending on investment returns and spending discipline.

- Comfortable lifestyle from 60 for a couple ($77,375 a year): Around $900,000 to $1.2 million combined.

$570K sits between the modest and comfortable benchmarks for a single homeowner retiring at 60. At $50,000 annual spending it is workable. At $60,000-plus it becomes tight without some part-time income in the early years.

Use the free Wealthlab super calculator to model your specific balance, spending and return assumptions.

What Is the Average Superannuation Balance at 60 in Australia?

The median super balance for Australians aged 60 to 64 is around $211,000 for women and $302,000 for men, based on recent ABS data. The mean (average) is higher, around $360,000 to $400,000 for men and lower for women, but is skewed by large balances at the top.

$570K at 60 is significantly above both the median and the mean for most Australians in this age group. If you are comparing yourself to these benchmarks and feeling behind, the truth is that $570K puts you ahead of the majority of Australians heading into retirement.

The relevant benchmark is not what the average person has. It is whether your balance, at your expected spending level, lasts for the retirement you want.

How Much Do You Need to Retire in Australia?

The answer depends on three variables: when you retire, how much you plan to spend, and whether you own your home.

ASFA’s February 2026 benchmarks for homeowners at age 67:

- Comfortable single: $630,000 in super

- Comfortable couple: $690,000 to $730,000 combined

- Modest single: $110,000 (the Age Pension covers most of the modest standard)

- Modest couple: $120,000

These figures assume the Age Pension supplements income from 67. They are not directly applicable to someone retiring at 60, where seven extra years of self-funding push the required balance higher.

The short answer for someone with $570K: you are close to the comfortable benchmark for retiring at 67, and workably positioned for retiring at 60 at moderate spending. The sweet spot for $570K is around $45,000 to $55,000 annual spending from 60, tightening the budget slightly in the early pre-pension years and having the Age Pension provide relief from 67.

Superannuation in Australia: What $570K Means in the Broader Context

Australia’s superannuation system is one of the largest pension fund pools in the world. As of 30 June 2025, Australians have $4.33 trillion invested in superannuation assets, making Australia the fourth largest holder of pension fund assets globally. The system was designed to reduce reliance on the Age Pension over time, and it is working: the proportion of retirees using super as their main income source has risen from 20% to 28% between 2014 and 2025.

From 1 July 2025, the superannuation guarantee increased from 11.5% to 12%, meaning employers now pay 12% of ordinary time earnings into super for all eligible employees. This is the final step in a decade-long phased increase from 9.5%.

For someone still working at 58 or 59 and looking to boost their balance before retiring at 60, this higher guarantee rate, combined with salary sacrifice contributions, can meaningfully increase a balance over the final working years.

What Is “$1,050 Less Super” About?

This query appears in the GSC data for this page and is worth explaining.

The SG increase from 11.5% to 12% on 1 July 2025 affected workers on total remuneration packages, where super is included in the total cost to company rather than paid on top of salary. For these workers, the higher SG rate meant their employer redirected more of their package to super, reducing their take-home pay.

For someone earning $210,000 on a total package, an extra 0.5% going to super equates to roughly $1,050 less in take-home pay per year. For someone on $100,000, it is approximately $500 less. The money has not disappeared; it is going into your super account. But if you noticed a pay reduction around July 2025 and are searching to understand why, this is likely the cause.

The silver lining: that extra money is accumulating in your super tax-effectively at 15%, compounding towards your retirement balance.

What Lifestyle Does $570K Support?

According to the ASFA Retirement Standard (February 2026), the comfortable lifestyle for a single homeowner requires $54,240 a year. A budget at $50,000 a year might look like:

| Category | Annual spend (approx.) |

|---|---|

| Groceries and food | $8,500 |

| Housing costs and rates | $5,000 |

| Healthcare and private health | $7,000 |

| Transport | $4,500 |

| Travel and leisure | $13,000 |

| Clothing and personal | $4,000 |

| Utilities and phone | $4,000 |

| Contingency buffer | $4,000 |

This is a comfortable lifestyle: private health cover, a reasonable car, regular travel, social activities and dining out. It is not extravagant, but it is genuinely comfortable for a homeowner with no debt.

What Happens at Age 67?

The Age Pension starts at 67 for anyone born on or after 1 January 1957. At $570K drawing down at $50,000 a year from 60, you would arrive at 67 with around $340,000.

That sits within the taper range for the Age Pension assets test (above $314,000 full threshold, below $695,000 cut-off for singles). You would likely receive a part pension of around $15,000 to $22,000 a year, depending on exact balance and other assets.

Combined with a reduced super drawdown, your total annual income from 67 would be in the range of $45,000 to $55,000, sustaining your pre-pension lifestyle comfortably.

Current 2026 Age Pension rates: approximately $29,754 a year for singles and $44,856 for couples (including supplements).

How to Make $570K Last Longer

Set up an account-based pension. Convert your super to a regular income stream rather than lump sum withdrawals. Tax-free, controlled, and keeps your balance invested and growing.

Stay in a balanced or growth option. A 30-year retirement horizon means inflation is your biggest long-term risk, not short-term volatility. In Episode 1 of the Wealthlab Podcast, Scott and Phil showed that a couple in a conservative portfolio ran out of money 15 years earlier than the same couple in a growth option, on identical spending. The investment mix decision matters enormously.

Consider part-time work in the early 60s. Even $15,000 to $20,000 a year from part-time work dramatically reduces super drawdown and preserves more for later. Many people find a gradual transition into retirement works better than a hard stop at 60.

Build a healthcare buffer. Medical expenses increase in later retirement. Budgeting for this from the start, rather than treating it as a surprise, keeps your financial plan on track.

Review your plan annually. Spending, investment returns, and life circumstances change. An annual review with a financial adviser keeps your drawdown strategy aligned with your actual situation.

FAQs: Retiring at 60 with $570K

Is $570K enough to retire at 60 in Australia?

Yes, for a single homeowner with moderate spending expectations around $45,000 to $55,000 a year. $570K is close to ASFA’s comfortable retirement benchmark and, with a balanced investment approach and part Age Pension from 67, supports a comfortable retirement well into your 80s.

How much superannuation do you need to retire at 60 in Australia?

For a comfortable lifestyle from age 60, around $650,000 to $850,000 for a single homeowner. For a modest lifestyle, $350,000 to $450,000 is workable. $570K falls between these ranges, suitable for comfortable retirement at moderate spending. These figures are higher than the ASFA 67-based benchmarks because of the extra self-funding years.

What is the average superannuation balance at 60 in Australia?

The median is around $211,000 for women and $302,000 for men aged 60 to 64. The mean average is higher but skewed by large balances. $570K is significantly above both the median and mean, putting you ahead of the majority of Australians in this age bracket.

How much do you need to retire in Australia?

ASFA’s comfortable retirement benchmarks at 67 are $630,000 for singles and around $690,000 to $730,000 for couples. For a modest retirement, much less is needed as the Age Pension covers most of the cost from 67. Retiring earlier than 67 requires a higher balance to cover the pre-pension self-funding years.

What is the superannuation guarantee rate in Australia?

From 1 July 2025, the superannuation guarantee is 12% of ordinary time earnings. This is the final step in a phased increase from 9.5% in 2021. Employers must pay this minimum rate into their employees’ super funds quarterly.

Why did my pay go down by about $1,050?

If you are on a total remuneration or cost-to-company package, the SG increase from 11.5% to 12% in July 2025 may have reduced your take-home pay as your employer redirected more of your package into super. The money has not been lost; it is in your super account growing tax-effectively.

Will I get the Age Pension with $570K at 60?

Likely a part pension when you reach 67, depending on how much you have drawn down by then. At $50,000 annual spending from 60, you would arrive at 67 with approximately $340,000. That puts you within the part pension taper range for a single homeowner, qualifying for a meaningful part payment.

How long will $570K last if I retire at 60?

At $50,000 annual spending and 5% net returns, approximately 20 years from age 60, taking you to around 80. With part Age Pension support from 67 onwards as the balance draws down, combined retirement income extends well into your mid to late 80s.

Ready to work out exactly what $570K means for your retirement? Book a free call with the Wealthlab team and get a retirement income plan built around your actual numbers.