Reaching $710,000 in super by age 60 is a solid achievement. The question is not really whether $710K is enough. It is how to manage it so it lasts for 25 to 30 years, how it compares to other balance levels, and what the Age Pension does to your picture from 67.

This guide covers what $710K can realistically support, how long it lasts at different spending levels, and answers the broader questions people are searching around this balance range.

Is $710K Enough to Retire Comfortably at 60?

Yes. $710K exceeds ASFA’s comfortable retirement benchmark of $630,000 for a single homeowner retiring at age 67. You have more than that, and you have it seven years earlier.

For most homeowners with modest to moderate spending expectations, $710K at 60 comfortably funds a retirement into your mid-80s without the Age Pension, and well into your 90s with it. The key variables are how much you spend annually and what your super stays invested in.

How Much Super Do I Need to Retire at 60?

This is the most-searched question on this page and worth answering directly.

For a single homeowner targeting a modest lifestyle, around $400,000 to $500,000 at age 60 provides reasonable coverage through to pension age at 67. For a comfortable lifestyle at the ASFA standard of $54,240 a year, you need closer to $700,000 to $900,000 at 60, depending on investment returns and how aggressively you draw down.

The ASFA benchmarks are calculated for people retiring at 67, not 60. Retiring seven years earlier means seven extra years of self-funding before pension support, which pushes the required balance higher. $710K sits comfortably in the range for a comfortable retirement from 60 for a single homeowner.

For a couple targeting the ASFA comfortable standard of $77,375 a year, $710K combined is workable but tighter. $710K each, or $1.4 million combined, gives much more room.

The free Wealthlab super calculator lets you model your specific balance and spending assumptions to get a clearer read on your own numbers.

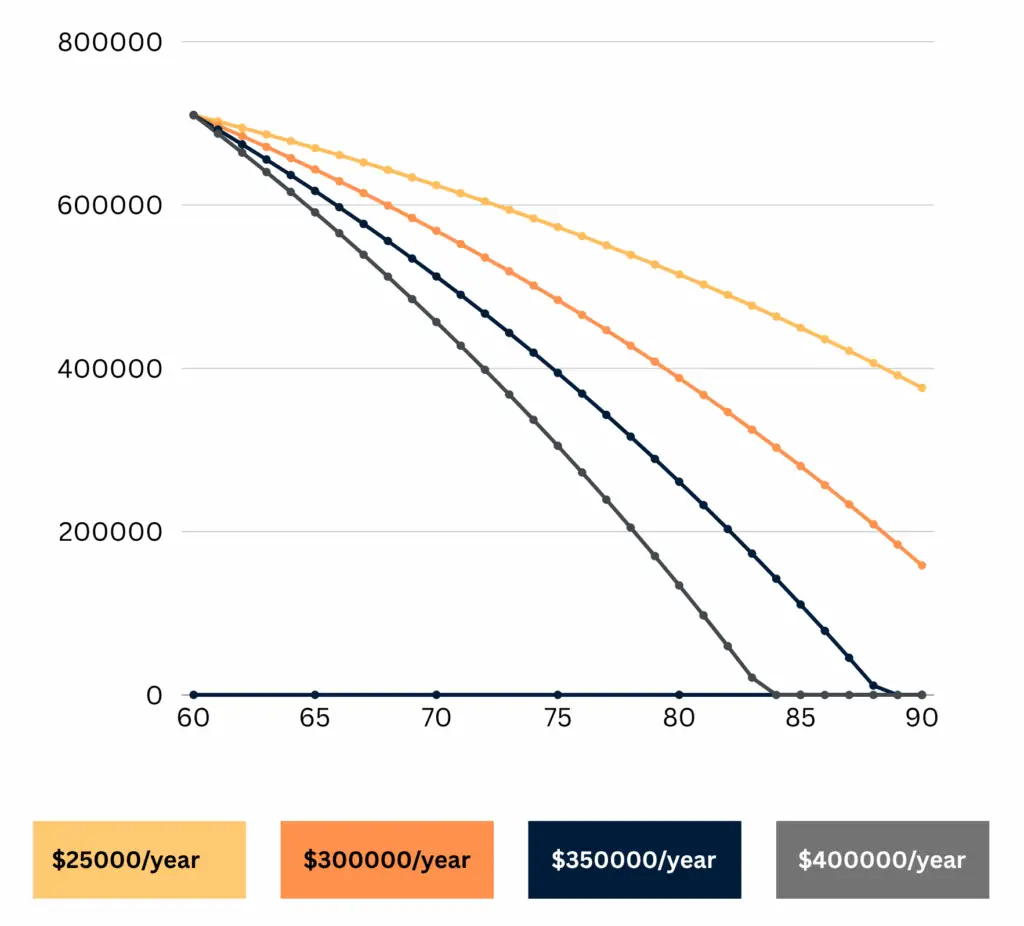

How Long Will $710K Last?

Assuming conservative investment returns of about 2.44% after inflation, here’s an estimate of how long your super might last at different annual spending levels:

| Annual Spending | Estimated Longevity |

|---|---|

| $25,000 | 31–33 years |

| $30,000 | 27–29 years |

| $35,000 | 24–26 years |

| $40,000 | 21–23 years |

These estimates assume you own your home and do not rely on super for mortgage or rent payments. Planning carefully ensures your $710K can support decades of retirement, even before Age Pension benefits start.Pension benefits start. 90s, particularly if you keep your spending moderate and integrate the Age Pension at 67.

Visualise how $710K declines from age 60 to 90 under different annual spending scenarios ($25K, $30K, $35K, $40K).

How Long Will $710K Last in Retirement?

Projection assuming 5% net annual return in an account-based pension, with Age Pension supplementing income from the mid-70s as the balance draws down:

| Annual spending | Years before balance is significantly reduced | With Age Pension top-up from ~75 |

|---|---|---|

| $45,000 | ~25 years (to age 85) | Well into 90s |

| $55,000 | ~18 years (to age 78) | Late 80s |

| $65,000 | ~13 years (to age 73) | Mid to late 80s |

| $77,000 (ASFA comfortable couple) | ~10 years (to age 70) | Early to mid 80s |

The Age Pension makes a substantial difference. Even at $710K, once your balance draws down past the assets test thresholds, a part pension kicks in. A single homeowner qualifies for a full Age Pension once assets fall below roughly $314,000. That point arrives sooner at higher spending levels but provides real income relief when it does.

What Does $710K in Superannuation Mean in Practice?

$710,000 in super at 60 puts you above the national average for that age bracket and above ASFA’s comfortable retirement threshold. In practical terms:

At $55,000 a year spending (close to the ASFA comfortable standard for singles), $710K at 60 with 5% net returns would look like this:

| Age | Starting balance | Withdrawal | Net growth | Ending balance |

|---|---|---|---|---|

| 60 | $710,000 | $55,000 | $32,750 | $687,750 |

| 63 | ~$620,000 | $55,000 | ~$28,250 | ~$593,250 |

| 67 | ~$490,000 | $40,000* | ~$22,500 | ~$472,500 |

| 72 | ~$320,000 | $35,000* | ~$14,250 | ~$299,250 |

| 77 | ~$170,000 | $30,000* | ~$7,000 | ~$147,000 |

*Reduced withdrawal from 67 as Age Pension supplements income.

By your late 70s, your balance is lower but the combined Age Pension and super drawdown income keeps you well above a modest lifestyle standard. $710K at 60 is a genuinely comfortable position.

Is $1 Million Enough to Retire at 60?

Yes, $1 million is more than enough to retire comfortably at 60 in Australia for most homeowners. At $65,000 to $70,000 annual spending and 5% net returns, $1 million at 60 would leave around $800,000 at age 67, which is well above the Age Pension full threshold but provides strong investment income without relying on the pension.

$1 million at 60 effectively funds a comfortable to generous retirement for most single Australians, and a comfortable retirement for most couples. The planning questions at this level shift from “is there enough money” to “how do I structure the investment mix and drawdown to be most tax-efficient and long-lasting.”

How Much Interest Does $1 Million Generate?

At a cash rate or term deposit rate of around 4 to 4.5% in 2026, $1 million in cash would generate roughly $40,000 to $45,000 a year in interest. That is below ASFA’s comfortable standard for singles ($54,240) and well below the couple’s comfortable standard ($77,375).

This is why keeping $1 million entirely in cash at retirement is generally not the optimal approach. A balanced investment portfolio targeting 6 to 7% gross returns (roughly 5% net after fees and inflation) generates more income and capital growth than cash alone, while still managing risk appropriately for a retiree. The interest-only approach also does not benefit from the capital portion of investment returns, which can make a significant difference over a 30-year retirement.

How Long Will $600,000 Last in Retirement in Australia?

At $50,000 annual spending and 5% net returns, $600,000 at age 60 would last approximately 18 to 20 years without any Age Pension support, taking you to around age 78 to 80. With a part Age Pension from your mid to late 70s as the balance draws down, combined income would sustain a modest to comfortable lifestyle into your mid to late 80s.

$600,000 at 67 (ASFA’s reference point for the comfortable standard) is right at the benchmark. At 60, it is somewhat below what you would ideally have for a comfortable retirement, though it is workable for a homeowner with moderate spending expectations and some flexibility.

How Long Will $2 Million Last in Retirement?

At $80,000 to $90,000 annual spending and 5% net returns, $2 million at 60 would sustain that lifestyle for well over 30 years, effectively until age 90 or beyond, without any Age Pension support.

At $2 million, the Age Pension is unlikely to be relevant in most scenarios, as the assets test thresholds mean your balance would remain above the taper point for many years. The planning questions at this level focus more on tax efficiency, estate planning and whether to keep super in accumulation or move to pension phase. Our superannuation page covers some of these strategies in more detail.

How to Stretch $710K Further

Draw super strategically. Set up an account-based pension rather than taking lump sums. This provides regular tax-free income and keeps most of your super invested and growing.

Maintain a balanced investment portfolio. A mix of growth and defensive assets protects against volatility while allowing long-term growth. Revisit your investment option annually and avoid moving entirely to cash, which loses ground to inflation over time.

Budget deliberately. At $710K, you can afford a comfortable lifestyle if you are thoughtful about it. Spending above $65,000 a year from 60 puts more pressure on the balance in the critical pre-pension years.

Consider part-time work in the early 60s. Even $20,000 to $25,000 a year in part-time income meaningfully reduces super drawdown in the first few years and preserves more for later.

Plan for healthcare costs. Budget for dental, optical and specialist care beyond Medicare. A basic private health insurance policy provides predictability and preserves your super for other priorities.

What Happens at Age 67?

At 67, most Australians become eligible for the Age Pension subject to income and assets tests. With $710K at 60 and seven years of drawdown, your balance at 67 will depend on your spending rate. At $55,000 a year, you would arrive at 67 with roughly $490,000, which sits above the full pension threshold but within the taper range for a part pension. At $65,000 a year, you would arrive at 67 with around $390,000, likely qualifying for a meaningful part pension.

Current Age Pension rates for 2026: approximately $29,754 a year for singles and $44,856 for couples (including supplements).

FAQs: Retiring at 60 with $710K in Australia

How much super do I need to retire at 60 in Australia?

For a comfortable lifestyle at the ASFA standard from age 60, around $700,000 to $900,000 provides strong coverage for a single homeowner. $710K sits comfortably in this range. For a modest lifestyle, $400,000 to $500,000 is generally workable from 60. Couples need more, typically $900,000 to $1.2 million combined for a comfortable lifestyle from 60.

Is $1 million enough to retire at 60 in Australia?

Yes, comfortably for most single homeowners and reasonably for couples. At $65,000 to $70,000 annual spending with moderate investment returns, $1 million at 60 funds a comfortable retirement well beyond age 90 for singles and into the late 80s for couples at higher spending levels.

How much interest does $1 million generate in Australia?

At current rates of around 4 to 4.5% in cash or term deposits, roughly $40,000 to $45,000 a year. A balanced investment portfolio targeting 5 to 6% net returns would generate more and preserve capital better over a 30-year retirement. Cash-only is generally not the optimal approach for a long retirement horizon.

How long will $600,000 last in retirement in Australia?

At $50,000 annual spending and 5% net returns, around 18 to 20 years from age 60, taking you to 78 to 80 without any Age Pension. Part pension support from the late 70s would extend combined retirement income into the mid to late 80s.

How long will $2 million last in retirement?

At $80,000 to $90,000 annual spending and 5% net returns, $2 million effectively funds retirement for 30-plus years from age 60, well past age 90 for most people. Age Pension is unlikely to be a major factor at this level given assets test thresholds.

What does $710K in superannuation mean for retirement?

$710K exceeds ASFA’s comfortable retirement benchmark for singles and provides a strong base for retiring at 60. At $55,000 annual spending with moderate investment returns and eventual Age Pension top-up, it funds a comfortable retirement well into your 80s.

How much super should I have at 60?

For a comfortable retirement from 60, around $700,000 to $900,000 for a single homeowner. For a modest lifestyle, $400,000 to $500,000. These figures are higher than the ASFA 67-based benchmarks because retiring at 60 adds seven years of self-funding before the Age Pension starts.

Want to see exactly how your $710K works across different spending and return scenarios? Book a free call with the Wealthlab team and get a retirement income model built around your actual numbers.