Retiring at 62 with $400,000 in super is possible for some Australians, but whether it works for you specifically depends on a handful of variables that matter far more than the balance alone: whether you own your home, whether you’re single or part of a couple, how much you want to spend in retirement, and how you plan to bridge the 5-year gap before the Age Pension starts at 67.

The short answer is that $400,000 gives a homeowning single a reasonable foundation for retiring at 62, particularly if spending is managed carefully and some part-time work or non-super savings support the early years. For a couple, it’s tighter. For a renter of any kind, it’s genuinely difficult without other assets.

Here’s the full picture.

The Core Challenge: The 5-Year Gap to Age Pension

Before running any numbers, it’s worth naming the central planning problem for anyone retiring at 62 in Australia.

The Age Pension becomes available at 67. Super becomes accessible at 60 (for anyone born after 30 June 1964). Retiring at 62 means 5 years of funding retirement entirely from your own savings, before any government support arrives.

During those 5 years, every dollar you draw from super is a dollar that won’t be earning returns for you later. And because you’re drawing from a $400,000 balance, even modest annual spending takes a meaningful chunk out of the principal in those early years.

This isn’t a reason not to retire at 62. But it’s the reason the plan needs to be built around those gap years specifically, not just the overall balance.

What Does $400,000 Actually Generate?

From age 60, super moved into pension phase earns investment returns and 0% tax on earnings (compared to 15% in accumulation phase). That tax-free growth is one of the most powerful features of the Australian super system.

At a net 5% annual return on $400,000, you’re generating roughly $20,000 per year in investment returns before any drawdown. That means if you draw $40,000 per year from super, you’re drawing $20,000 from capital each year in addition to consuming the investment returns.

Over the 5-year gap to Age Pension at 67, drawing $40,000 per year from a $400,000 balance at 5% net return would reduce your balance to approximately $310,000 to $325,000 by age 67, depending on the exact sequence of returns.

At that point, with a balance around $310,000 to $325,000 and a homeowning single’s Age Pension cut-off of $722,000 in assessable assets (as at March 2026), you’d likely qualify for close to the full Age Pension of $31,223 per year. That significantly reduces the annual drawdown required from super from 67 onwards, extending how long the remaining balance lasts.

These figures are illustrative projections only. Individual outcomes depend on actual investment returns, spending, tax, inflation, and personal circumstances. Past performance is not a reliable indicator of future performance.

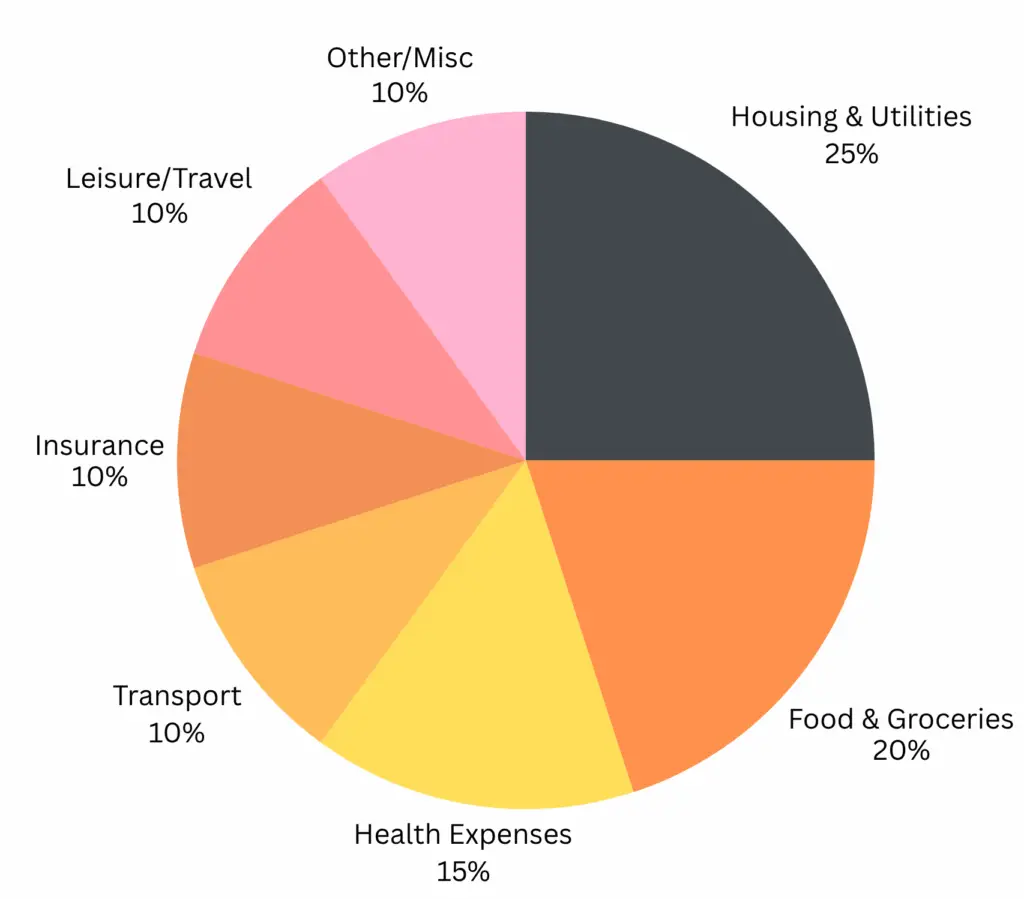

Can I Retire at 62? Budget Breakdown for $25,000 Per Year

A practical $25,000 annual budget might look like this:

| Category | Percentage of budget |

|---|---|

| Housing and utilities | 25% |

| Food and groceries | 20% |

| Healthcare | 15% |

| Transport | 10% |

| Insurance | 10% |

| Leisure and travel | 10% |

| Miscellaneous | 10% |

Can I Retire at 62? Home Ownership Advantage

Owning your home can make a significant difference. Without rent or mortgage payments, your super stretches much further. Mortgage-free retirees can combine super with part-time work or Age Pension support to maintain a stable and fulfilling lifestyle.

If you rent, consider downsizing or relocating to reduce expenses, which can help your super last longer.

Scenario 1: Single Homeowner Retiring at 62 with $400,000

This is the most viable scenario for $400,000 at 62.

The income question: ASFA’s comfortable retirement standard for a single homeowner is $54,837 per year (February 2026). A modest retirement standard is around $35,199 per year. The gap years between 62 and 67 are the most financially demanding part of the plan, because you’re funding the full cost of living from super alone.

If you can genuinely live on $35,000 to $40,000 per year as a homeowner with no mortgage, $400,000 gives you roughly 5 years of funding before Age Pension support arrives at 67. From 67, the part or full Age Pension supplements your super drawdown and the pressure on your balance reduces considerably.

The realistic picture: A homeowning single who retires at 62 on $400,000, draws $38,000 per year, and earns a net 5% return, would arrive at 67 with approximately $300,000 to $320,000 remaining. At that balance, they’d likely qualify for a substantial part pension or full Age Pension (subject to the assets and income tests applying at that time). Combined income from super drawdown plus pension could sustain a modest-to-comfortable lifestyle through to late 80s or beyond.

What makes it work: Keeping spending disciplined in the early gap years, having a small cash buffer outside super to avoid forced selling in a down market, and structuring the super drawdown to qualify for maximum Age Pension entitlement at 67.

Scenario 2: Couple Retiring at 62 with $400,000 Combined

For a couple with $400,000 combined super, retiring at 62 is considerably tighter.

ASFA’s comfortable retirement standard for a couple is $77,375 per year. Even the modest standard is $50,866 per year. A couple drawing $50,000 per year from a $400,000 balance at 5% net return would exhaust the balance in approximately 10 to 12 years, reaching 72 to 74 with very little super left. From 67, the couple’s Age Pension of up to $47,070 per year (combined, as at March 2026) provides meaningful support but doesn’t fully replace the super income they’ve been drawing.

For a couple, $400,000 combined at 62 requires either significantly reduced spending expectations, one partner continuing to work part-time, or both. The scenario can be made to work but it requires more careful management than a single homeowner at the same balance.

Where it works better: If the $400,000 is split reasonably evenly between both partners’ super accounts, and each qualifies for a part Age Pension separately from 67, the combined pension entitlement is higher than one partner qualifying alone. Structuring super between partners with Age Pension eligibility in mind is one of the key planning levers for couples in this position.

Scenario 3: Single Renter Retiring at 62 with $400,000

This is the most difficult of the three scenarios. Rent adds $18,000 to $30,000 or more per year on top of living costs, which dramatically accelerates how quickly a $400,000 balance is drawn down.

A single renter spending $55,000 per year (covering rent plus modest living costs) would deplete $400,000 in approximately 9 to 11 years, reaching approximately 71 to 73 with little remaining. Rent Assistance is available to Age Pension recipients who rent privately (up to approximately $157 per fortnight as at 2026 for singles), but it doesn’t come close to covering actual rental costs.

For a renter with $400,000 at 62, retiring fully is very high risk. A semi-retirement model, with part-time work supplementing income through the gap years, is a significantly more sustainable approach. Alternatively, part of the $400,000 might be used to purchase a more affordable property, though the trade-offs of doing so at 62 need to be carefully modelled.

The Age Pension: A Bigger Safety Net Than Most People Realise

One dynamic that works in favour of a $400,000 retirement at 62 is the Age Pension interaction at 67.

Because you’ve been drawing down your super balance for 5 years before the pension becomes available, your assessable assets at 67 are considerably lower than your starting balance. A lower balance at 67 means more Age Pension entitlement, which reduces the annual drawdown required from super and extends how long the remaining balance lasts.

As at March 2026, the Age Pension rates and key homeowner thresholds are:

- Full single Age Pension: $1,200.90 per fortnight ($31,223 per year)

- Full couple Age Pension (combined): $1,810.40 per fortnight ($47,070 per year)

- Full pension assets test threshold (single homeowner): $321,500

- Part pension cut-off (single homeowner): $722,000

- Full pension assets test threshold (couple homeowners): $481,500

- Part pension cut-off (couple homeowners): $1,085,000

Current as at March 2026. These figures are set by the Australian Government and are typically updated each March and September. Source: Services Australia

Phil and Dan covered how the Age Pension assets test works in practice in Episode 10 of the Wealthlab podcast, “How the Age Pension Really Works.” The episode includes real worked examples of how drawing down super between 60 and 67 can actually improve your Age Pension position at 67, sometimes significantly.

What You Spend in Retirement Matters as Much as the Balance

The old post on this topic used a 2.5% investment return assumption, which is very conservative and understates what most diversified super funds deliver over time. But the more important variable is spending.

The difference between spending $35,000 and $45,000 per year from a $400,000 balance over the 5-year gap to Age Pension is $50,000 in total drawdown. That’s more than 12% of the starting balance. At 5% net returns, the balance at 67 is approximately $50,000 to $60,000 higher in the lower-spending scenario, which translates directly into better Age Pension eligibility and a longer-lasting balance through retirement.

For a $400,000 retirement at 62 to work well, the spending discipline in the first 5 years genuinely matters. After 67, the Age Pension provides a floor and the pressure reduces.

The realistic retirement spending targets for a homeowner (ASFA, February 2026) are:

- Modest lifestyle, single: ~$35,199 per year

- Comfortable lifestyle, single: ~$54,837 per year

- Modest lifestyle, couple: ~$50,866 per year

- Comfortable lifestyle, couple: ~$77,375 per year

Source: ASFA Retirement Standard, February 2026. All figures assume home ownership and are updated quarterly.

A $400,000 balance at 62 realistically supports a single homeowner targeting somewhere between the modest and comfortable standards, particularly if part-time income or non-super savings supplement the gap years.

Strategies That Improve the Outcome

Keep working part-time for 2 to 3 years. Even $15,000 to $20,000 per year from part-time or casual work dramatically reduces the drawdown on your $400,000 in the early years. This alone can add $75,000 to $100,000 to your balance at 67 compared to full retirement at 62.

Build a cash buffer outside super before retiring. Having 12 to 24 months of living expenses in cash or a savings account outside super protects you from having to sell super investments at a loss if markets fall in your first year or two of retirement. Scott covered why this matters in Episode 1 of the Wealthlab podcast, “Why Playing It Safe in Retirement Can Cost You More”: the same 6% average return can fund retirement to your late 90s or run out 15 years earlier depending on when in the sequence that return comes.

Review your investment mix. At 62 with a 25 to 30-year retirement ahead of you, being too conservative too early costs you real money in foregone growth. Being too aggressive risks a badly timed market fall wiping your early retirement balance. A blended approach, with 12 to 24 months of expenses in cash or defensive assets and the remainder in growth-oriented options, is the most common sensible structure.

Understand your Age Pension position at 67 before you retire. If your plan involves drawing from $400,000 over the gap years, model what your assessable assets will look like at 67 and what Age Pension entitlement that generates. In some cases, a small amount of planning around which assets to draw first can materially improve the pension outcome.

Consider delaying retirement by even one or two years. Retiring at 64 instead of 62 with $400,000 in super adds roughly 2 more years of contributions and investment growth, reduces the gap to Age Pension from 5 years to 3, and typically adds $80,000 to $120,000 to the balance at retirement. That changes the sustainability of the plan considerably. We explored this trade-off in detail in our guide on when is the best time to retire in Australia.

Run Your Own Numbers

Before making any decision, it’s worth seeing what your own numbers look like. Our free Wealthlab super calculator lets you model your projected balance at different retirement ages and see how different spending scenarios affect how long your money lasts.

FAQs

Can I retire at 62 with $400K in super in Australia?

It depends primarily on whether you own your home, whether you’re single or part of a couple, and how much you expect to spend. A single homeowner targeting a modest-to-comfortable lifestyle of around $35,000 to $40,000 per year has a reasonable foundation with $400,000 at 62, particularly once the Age Pension begins supplementing income from 67. A couple at $400,000 combined is tighter and likely requires part-time work or reduced spending in the early years. A renter at any level finds it genuinely difficult without additional assets.

How long will $400,000 in super last if I retire at 62?

At a net 5% annual return and $40,000 per year in withdrawals, $400,000 would last approximately 14 to 16 years before depletion, taking you to age 76 to 78. However, this doesn’t account for the Age Pension becoming available at 67, which reduces the required super drawdown and extends the balance significantly. A single homeowner qualifying for a part or full Age Pension at 67 may find that $400,000 at 62 provides sustainable income well into their late 80s, depending on actual investment returns and spending. These are illustrative projections only. Individual outcomes vary.

Is $400,000 enough to retire in Australia?

Whether $400,000 is enough depends on your age at retirement, home ownership, lifestyle expectations, and other income sources. For someone retiring at 67 who already qualifies for the Age Pension, $400,000 in super combined with a full or part pension can support a reasonable lifestyle, particularly as a homeowner. For someone retiring at 62 with 5 years before pension eligibility, $400,000 requires disciplined spending management through the gap years. The ASFA comfortable retirement benchmark requires $630,000 for a single at 67 (February 2026), so $400,000 is below that standard but workable with careful planning.

What is the Age Pension threshold for a homeowner at 67?

As at March 2026, a single homeowner with assessable assets below $321,500 qualifies for the full Age Pension ($31,223 per year). The part pension tapers to zero at $722,000 in assessable assets for a single homeowner. For a couple homeowner, the full pension threshold is $481,500 combined and the cut-off is $1,085,000 combined. Super in pension phase is included in assessable assets. These thresholds are updated each March and September. Source: Services Australia.

Should I delay retirement past 62 if I have $400,000 in super?

Delaying from 62 to 64 typically adds $80,000 to $120,000 to a $400,000 balance through continued contributions and investment growth (depending on your contribution rate and returns), and reduces the gap to Age Pension from 5 years to 3. Whether those 2 extra years of work are worth the financial benefit is a personal decision. For someone in poor health or a high-stress job, retiring sooner with a tighter plan may be the better choice. For someone enjoying work and in good health, waiting a couple of extra years produces a meaningfully more comfortable retirement. The decision is worth modelling with real numbers before committing.

Can I retire at 62 as a couple with $400,000 combined?

It’s possible but tight. A couple targeting even a modest lifestyle of approximately $50,866 per year (ASFA February 2026) would draw from a $400,000 balance at a rate that depletes it within 10 to 12 years, before the Age Pension fully offsets the shortfall. For a couple, this scenario works best if one partner continues part-time work for 2 to 3 years, or if the couple has significant non-super assets. Structuring super between both partners’ accounts to optimise Age Pension eligibility from 67 is also important. An adviser can model the couple-specific numbers and identify the most effective structure.

Getting the Plan Right Before You Pull the Trigger

Deciding to retire at 62 with $400,000 is one of the biggest financial decisions you’ll make, and the difference between a plan that works and one that runs into trouble often comes down to details that aren’t visible from the balance alone: how your super is invested, how you structure drawdowns, when you apply for the Age Pension, and whether your spending plan reflects how you’ll actually live.

At Wealthlab, we work through exactly these scenarios with people approaching retirement. If you’d like to understand what retiring at 62 could look like with your specific numbers, book a free chat with the team. No jargon, no pressure.