If you are 62 and looking at a super balance of $465,000, you are probably asking the same question thousands of Australians search every month: can I retire at 62 and will $465K be enough to live comfortably?

The good news is that yes, you can retire at 62 with $465K, especially if you own your home, manage your expenses carefully, and plan well for the early years before the Age Pension starts at 67.

Retiring at 62 means your super needs to support you for at least five years before any government support kicks in. After that, the Age Pension can help stretch your money even further.

Let’s break down how retirement works at 62, how far $465K can go, and how to plan a retirement you feel confident about.

Understanding Retirement at 62 in Australia

The retirement age in Australia for the Age Pension is 67, but many Australians choose to retire earlier, often at 60 to 62, when they can access their superannuation.

If you retire at 62, your income will come from:

- Your superannuation via lump sums or an account-based pension

- Personal savings or investments

- Potential part-time or casual work

- The Age Pension, but only once you reach 67

This means the years 62 to 67 are your self-funded years, and planning how to bridge that gap is critical.

For a full breakdown of how much income you actually need in retirement, see our guide on comfortable retirement in Australia.

Where Does $465K Sit by Australian Standards?

Before looking at the projections, it is worth understanding where $465,000 actually sits relative to what Australians typically have.

ASFA data from the ATO shows the average super balance for the 60 to 64 age group is approximately $430,000 to $450,000 for men and $330,000 to $350,000 for women. At $465,000, you are above the national average for your age group.

ASFA’s February 2026 Retirement Standard benchmarks $630,000 for a comfortable retirement for a single homeowner and $730,000 for a couple, measured at age 67. At 62, retiring five years earlier, $465,000 is below those targets but with a 5% investment return and disciplined spending, you can track close to these benchmarks by the time you actually reach 67.

The important context: most Australians retire on less than you have. $465K gives you real options.

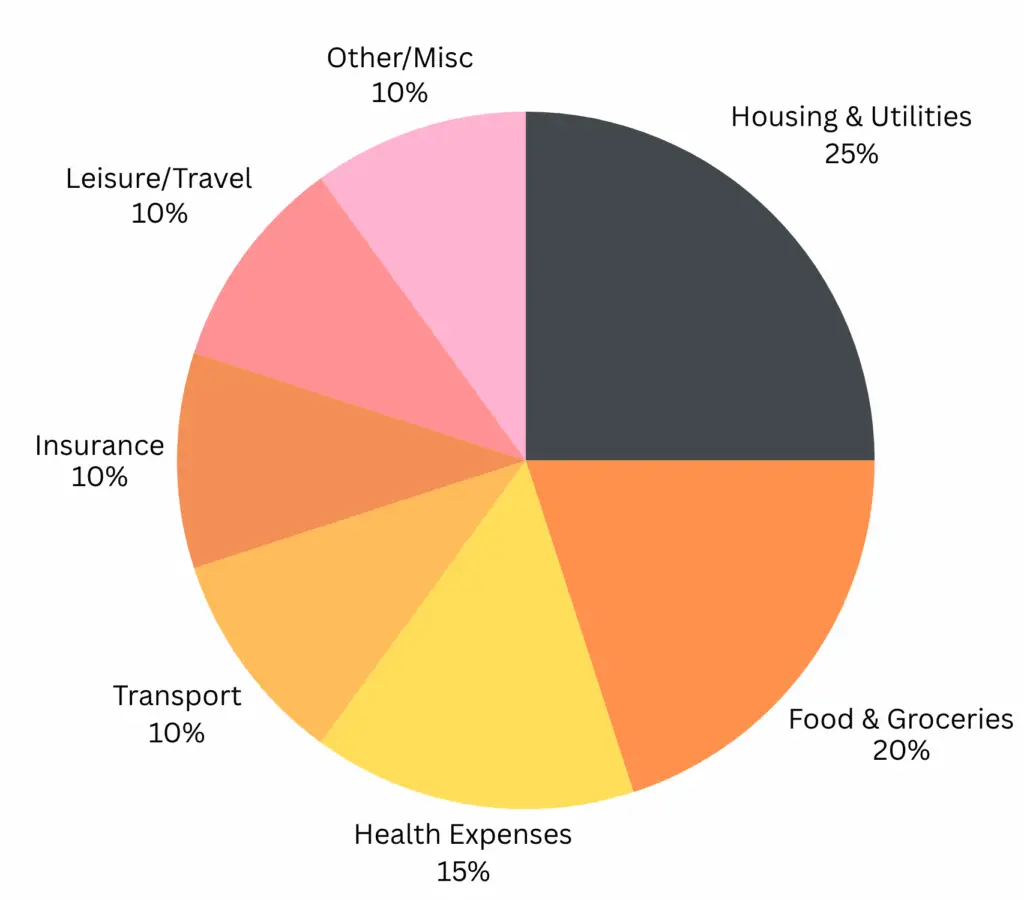

Example Budget: Retiring at 62 on $25,000 Per Year

If you aim to spend around $25K per year, here’s what a realistic and sustainable retirement budget might look like:

| Category | % of Annual Budget |

|---|---|

| Housing & Utilities | 25% |

| Food & Groceries | 20% |

| Healthcare | 15% |

| Transport | 10% |

| Insurance | 10% |

| Travel & Leisure | 10% |

| Miscellaneous | 10% |

This structure focuses on essentials, yet still allows for occasional travel and leisure a realistic lifestyle for many Australians retiring at 62.

How Long Will $465K Last If I Retire at 62?

The original projections on this page used a 3% return assumption, which reflects a conservative or cash option. A balanced account-based pension invested in a moderate growth option has historically returned around 5% per annum net of fees. Here are updated projections at two spending levels:

Scenario A: $25,000 per year at 5% return

| Age | Opening balance | Annual drawdown | 5% return | Closing balance |

|---|---|---|---|---|

| 62 | $465,000 | $25,000 | $22,000 | $462,000 |

| 63 | $462,000 | $25,000 | $21,850 | $458,850 |

| 64 | $458,850 | $25,000 | $21,693 | $455,543 |

| 65 | $455,543 | $25,000 | $21,527 | $452,070 |

| 66 | $452,070 | $25,000 | $21,354 | $448,424 |

| Age 67 | $448,424 | Age Pension eligibility |

At $25,000 per year with a 5% return, $465K barely moves over the five-year gap. You arrive at 67 with approximately $448,000, essentially the same balance you started with.

Scenario B: $35,000 per year at 5% return

| Age | Opening balance | Annual drawdown | 5% return | Closing balance |

|---|---|---|---|---|

| 62 | $465,000 | $35,000 | $21,500 | $451,500 |

| 63 | $451,500 | $35,000 | $20,825 | $437,325 |

| 64 | $437,325 | $35,000 | $20,116 | $422,441 |

| 65 | $422,441 | $35,000 | $19,372 | $406,813 |

| 66 | $406,813 | $35,000 | $18,591 | $390,404 |

| Age 67 | $390,404 | Age Pension eligibility |

At $35,000 per year, you arrive at 67 with approximately $390,000. That is above the full Age Pension threshold for a single homeowner ($314,000) but you will move below it within a few years of continued drawdown, progressively qualifying for a part pension and then eventually the full pension.

These are estimates. Actual outcomes depend on investment performance, fee structures, and the timing of withdrawals.

Example Budget: Retiring at 62 on $25,000 Per Year

If you aim to spend around $25,000 per year, here is what a realistic and sustainable retirement budget might look like:

| Category | Percentage of annual budget |

|---|---|

| Housing and utilities | 25% |

| Food and groceries | 20% |

| Healthcare | 15% |

| Transport | 10% |

| Insurance | 10% |

| Travel and leisure | 10% |

| Miscellaneous | 10% |

This structure focuses on essentials yet still allows for occasional travel and leisure, a realistic lifestyle for many Australians retiring at 62 who own their home.

The ASFA modest retirement standard for a single homeowner in 2026 is $36,700 per year. At $25,000, you are spending below that standard, but the Age Pension from 67 closes the gap. Once the full Age Pension of $31,223 per year starts, your combined income from super drawdown and pension can comfortably meet or exceed the modest standard.

Why Homeownership Matters in Retirement

Owning your home is one of the biggest advantages when retiring early. Without rent or mortgage payments, your fixed expenses drop dramatically, allowing your $465K to last far longer.

Your home is also exempt from the Age Pension assets test regardless of its value. This means owning a $1 million home does not reduce your Age Pension entitlement at all. The assets that count are financial assets like super, bank accounts, investments, and vehicles.

If you do not own your home, you may want to consider downsizing, relocating to a regional area, using the downsizer contribution (up to $300,000 per person into super), or supplementing income with light part-time work. These strategies help reduce pressure on your super, especially before the Age Pension starts at 67.

What the Age Pension Adds From 67

From 20 March 2026, the full Age Pension rates are:

| Fortnightly | Annual | |

|---|---|---|

| Single (full pension) | $1,200.90 | ~$31,223 |

| Couple combined (full pension) | $1,810.40 | ~$47,070 |

Source: Services Australia: Age Pension rates

The assets test thresholds for homeowners from March 2026 are:

| Full pension below | Pension cuts out above | |

|---|---|---|

| Single | $314,000 | $695,500 |

| Couple | $470,000 | $1,075,500 |

With $448,000 at 67 (Scenario A), you are above the full pension threshold but eligible for a part pension. As your balance continues to reduce through your 70s, your pension entitlement grows. With $390,000 at 67 (Scenario B), you are moderately above the threshold but will cross below it within a few years, progressively qualifying for more pension support.

Many retirees also qualify for the Commonwealth Seniors Health Card, which provides concessions on pharmaceutical costs, utilities, healthcare, and transport. This reduces your real cost of living significantly and is often overlooked in retirement planning.

Scott and Phil walked through how the Age Pension assets test actually works in real scenarios in Episode 10 of the Wealthlab Podcast: How the Age Pension Really Works With Real Case Studies. Worth listening to if you want to understand exactly how drawdown timing affects your entitlements.

Managing Your Super Wisely Between 62 and 67

The years from 62 to 67 are the most important in this retirement scenario. Your super needs to support you fully during these years. Here is how to make it work.

1. Convert your super to an account-based pension

This gives you flexible and regular income, tax free withdrawals after age 60, and continued investment growth inside the super system. In pension phase, your fund’s investment earnings are taxed at 0% compared to 15% in accumulation phase. On $465,000 earning 5%, that is $23,250 in annual earnings with zero tax instead of $3,488. Convert on day one of retirement.

2. Invest for growth, not just safety

Even in retirement, keeping a meaningful portion of your balance in a balanced or moderate growth option helps your money last significantly longer. As Scott covered in Episode 1 of the Wealthlab Podcast, a conservative portfolio often depletes faster than a growth portfolio over a long retirement because the returns cannot keep pace with drawdowns and inflation.

The right structure is to hold 12 to 18 months of living expenses in cash for stability and keep the remainder in a balanced growth option. This gives you the security of knowing you can always meet near-term expenses without selling growth assets at a bad time, while the bulk of your balance continues to compound.

3. Avoid large lump sum withdrawals

Major withdrawals early in retirement permanently remove capital that could otherwise compound for decades. Keep your spending controlled and matched to your actual budget until the Age Pension provides additional support from 67.

4. Consider part-time work

Even one day per week of paid work can reduce pressure on your super and extend its lifespan significantly. Drawing $10,000 to $15,000 per year from work instead of from super during the 62 to 67 gap preserves tens of thousands in compounding capital. Many Australians in their early 60s find that light work also provides social connection and purpose, making it a valuable part of semi-retirement rather than a financial necessity.

5. Check your Age Pension eligibility at 67

Apply for the Age Pension up to 13 weeks before your 67th birthday. If your claim is processed before your birthday, payments start from the day you turn 67. Waiting until after your birthday to apply means payments start from the submission date, not your birthday. Months of pension income can be forfeited by not planning the application in advance.

The Investment Option Decision: Why It Matters More Than You Think

This point deserves its own section because it is one of the most consequential decisions a retiree makes and most people get it wrong.

The projections above use a 5% return, which reflects a balanced or moderate growth portfolio. If you move to a conservative option or cash at retirement, you might get 2 to 3%. On $465,000 over five years, the difference between a 3% return and a 5% return is approximately $50,000 to $60,000 in lost compounding capital.

Over a 25-year retirement, that difference is vastly larger.

The instinct to “protect” your super by moving to cash or conservative at retirement is understandable but usually counterproductive. The real risk in a long retirement is not a short-term market fall. It is running out of money in your 80s because your returns could not keep pace with inflation and drawdowns.

The solution is not to go fully into growth and expose yourself to a market crash in year one of retirement. It is to hold a cash buffer covering one to two years of living expenses and keep the rest in a balanced option. This structure protects you against short-term volatility while keeping your long-term returns meaningful.

Want to see how different investment options affect how long your $465K lasts? Run your own numbers through the Wealthlab super calculator.

Planning Tips to Retire at 62 With Confidence

You can retire at 62 with $465K if you:

- Own your home with no mortgage

- Budget realistically around $25,000 to $35,000 per year

- Use a smart drawdown strategy via an account-based pension

- Keep your super invested in a balanced option with a cash buffer

- Plan the 62 to 67 self-funded gap carefully

- Apply for the Age Pension at 67 proactively

- Reassess your spending every few years as your circumstances change

Retirement age in Australia may be 67 for the pension, but you can absolutely retire earlier if you plan well.

FAQs: Can I Retire at 62 With $465K in Super?

Can I retire at 62 with $465K in super?

Yes. At $25,000 per year with a 5% investment return, your balance barely moves over the 62 to 67 gap and you arrive at 67 with approximately $448,000 still invested. At $35,000 per year you arrive with around $390,000. In both cases you qualify for Age Pension support from 67, which progressively supplements your income as your balance reduces.

How long will $465K last if I retire at 62?

With a 5% investment return and $25,000 per year in spending, $465K could last 30 or more years because the investment return nearly matches the drawdown rate. At $35,000 per year, your balance still grows slightly before reducing from your mid-70s onwards. Once the Age Pension supplements your income from 67, the combined income stream extends the sustainability of your super significantly.

Will I get the Age Pension at 67 with $465K?

If you are drawing $25,000 per year from 62, you arrive at 67 with approximately $448,000, which is above the full pension threshold for a single homeowner ($314,000). You will receive a part pension that grows as your balance reduces through your 70s. If you are drawing $35,000 per year, you arrive at 67 with approximately $390,000 and will cross below the full pension threshold within a few years, qualifying for increasing pension support.

What is the Age Pension from March 2026?

From 20 March 2026, the full Age Pension pays $1,200.90 per fortnight ($31,223 per year) for singles and $1,810.40 per fortnight ($47,070 per year) for couples combined. Eligibility depends on the assets and income tests administered by Services Australia.

What is the best investment option when retiring at 62?

For most retirees at 62, a balanced or moderate growth option with a separate cash buffer covering 12 to 18 months of expenses is the most appropriate structure. Going fully conservative or into cash risks running out of money through low returns, which is often more damaging over a 25-year retirement than a short-term market fall. An account-based pension in a balanced option with a cash buffer provides both security and growth.

What if I am retiring as a couple with $465K combined?

With $465,000 combined between two partners, say $232,500 each, the scenario requires more discipline. Combined spending of $35,000 to $40,000 per year during the 62 to 67 gap is manageable but tight. The couple’s full Age Pension from 67 ($47,070 per year combined) provides a strong income floor that makes the long-term picture sustainable, particularly for homeowners. Our guide on can couples combine super in Australia covers the strategies for managing two super accounts together.

Retiring at 62 with $465,000 is absolutely achievable and the maths is stronger than most people realise when you use a realistic investment return rather than a pessimistic one. With a sensible drawdown rate, an account-based pension in pension phase, and a clear plan for the 62 to 67 gap, $465K can support a modest to moderate lifestyle now and a comfortable one once the Age Pension starts at 67.

At Wealthlab, we help Australians turn their super into a clear, structured retirement income plan whether their balance is above or below the ASFA benchmarks. Book a free 15-minute call to talk through your numbers,