The short answer is yes, retiring at 60 with $720,000 in super is workable for many Australians. But the longer answer matters more, because 60 is early. You’ll be funding your own retirement for up to seven years before the Age Pension becomes available at 67, and potentially 25 to 30 years of retirement overall. That’s a long time to make $720K last.

The good news is that $720K is a strong starting point, well above the average Australian retirement balance, and with the right drawdown strategy it can comfortably carry you through your 60s and well into your 80s and beyond. Here’s what you actually need to think through.

The First Challenge: The 7-Year Gap Before Age Pension

One thing that catches a lot of early retirees off guard is the Age Pension age. In Australia, you can’t access the Age Pension until you turn 67. If you retire at 60, your super needs to carry you entirely for those first seven years.

At a drawdown rate of around $55,000 to $60,000 a year for a single retiree, seven years before the pension costs you roughly $385,000 to $420,000 from your $720K balance. That’s before investment returns are factored in, which is why keeping your super working in a well-structured investment mix during retirement matters just as much as the balance itself.

Once the Age Pension kicks in at 67, it can significantly extend how long your super lasts, and understanding how it interacts with your super is one of the most valuable things you can do before you retire. The current maximum rates (as at April 2026, per Services Australia) are:

- Single: approximately $31,223 per year

- Couple (combined): approximately $47,070 per year

Whether you receive the full Age Pension, a part pension, or nothing at all depends on your assets and income at the time. With $720K in super, most retirees would receive at least a part pension once their balance has drawn down over time.

Current as at April 2026. Age Pension rates are updated by the Australian Government each March and September. Figures sourced from Services Australia.

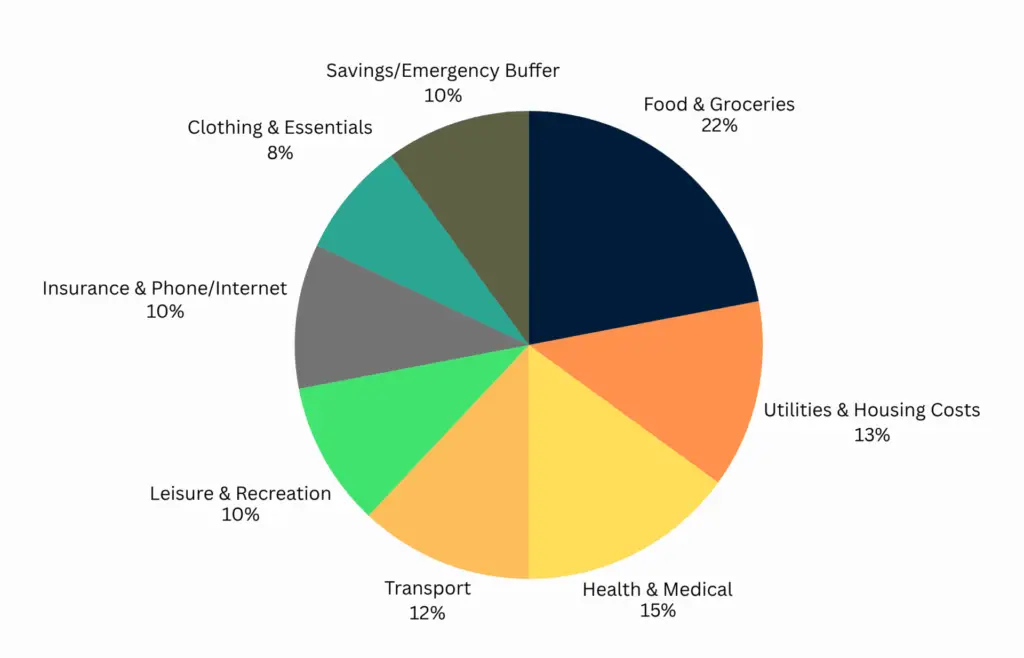

Example Budget for $30K Annual Retirement Lifestyle

Planning to live on around $30K/year? Here’s a realistic allocation:

| Category | % of Budget |

|---|---|

| Food & Groceries | 22% |

| Utilities & Housing Costs | 13% |

| Health & Medical | 15% |

| Transport | 12% |

| Leisure & Recreation | 10% |

| Insurance & Internet | 10% |

| Clothing & Essentials | 8% |

| Emergency Fund/Savings | 10% |

This budget supports a modest but comfortable lifestyle, especially if you’re living in a lower-cost area or regional town.

What Kind of Income Can $720K Generate?

A common starting point is the ASFA Retirement Standard, which estimates the annual income needed for a comfortable retirement in Australia:

- Single: around $51,278 per year (as at December 2024, ASFA)

- Couple: around $72,148 per year

With $720K, a single retiree spending around $50,000 to $55,000 a year is in a realistic position, assuming the super stays invested and generates a reasonable return. A couple spending $65,000 to $70,000 combined would be drawing harder on the balance but could still be workable, especially as the Age Pension progressively supplements income from 67.

Owning your home outright makes a significant difference. Without rent or mortgage repayments, the same super balance stretches considerably further.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees, and current government policy. This is general information, not personal advice.

The Withdrawal Rate Question

A commonly referenced guide is withdrawing no more than 4% to 5% of your balance per year in retirement. On $720K, that works out to around $28,800 to $36,000 a year at the lower end. That sounds modest, but the minimum drawdown rules for account-based pensions change with age, and once the Age Pension supplements your income the pressure on your super eases considerably.

The real risk for retirees with a 25 to 30 year horizon isn’t running out quickly early on. It’s being too conservative with your investment allocation and watching inflation quietly erode your purchasing power. Scott and Phil covered this in detail in episode 1 of the Wealthlab Podcast, walking through a real comparison of growth versus conservative portfolios over a long retirement. The numbers are eye-opening.

Strategies Worth Knowing About at 60

Transition to Retirement

If you haven’t fully stopped work yet, a transition to retirement (TTR) pension lets you access your super while still working, which can allow you to reduce hours, top up your income, and manage tax more effectively in the lead-up to full retirement. This isn’t right for everyone, but understanding how superannuation works in this phase is worth your time before making any moves.

Keeping Your Investment Mix Working

Retiring at 60 with a 25 to 30 year retirement ahead of you means your super still has a long investment horizon. A portfolio that’s too conservative too early can actually reduce how long your savings last, rather than protect them. The right balance between growth and defensive assets is one of the most important decisions to get right, and it’s very individual.

Account-Based Pension

When you retire, moving your super into an account-based pension shifts the earnings to a tax-free environment. This is a meaningful change from the 15% tax on earnings inside the accumulation phase, and it’s one of the less obvious financial advantages of actually retiring rather than just reducing hours.

Keeping an Eye on the Assets Test

As your super balance draws down, more of it may fall under the Age Pension assets test thresholds over time. The family home is exempt from the assets test, which is a significant advantage for homeowners. For homeowner couples, the lower assets test threshold for a part pension currently sits at $1,045,500 (as at April 2026, Services Australia). Even if you’re above the threshold at 67, drawdown over time may shift your entitlement.

These figures are set by the Australian Government and are typically updated each March and September.

Want to Run Your Own Numbers?

Everyone’s retirement looks different. Your spending, health, whether you’re single or part of a couple, whether you own your home, and what your super is invested in all change the picture. Before making any decisions, it’s worth putting some numbers together.

Try the free Wealthlab super calculator to get a rough sense of how your balance, drawdown rate and Age Pension might fit together over time.

FAQs: Retiring at 60 with $720K in Australia

Is $720K enough to retire at 60 in Australia?

For many Australians, $720K is a workable starting point, particularly for those who own their home. The key variable is spending. A retiree drawing $50,000 to $55,000 a year from $720K, with the super remaining invested, is in a very different position to one drawing $70,000 a year from day one. The Age Pension at 67 also eases pressure on the balance from that point.

How long will $720K last in retirement?

That depends on your drawdown rate, investment returns, fees and inflation. A retiree drawing around $50,000 a year from $720K with modest returns and Age Pension support from 67 could reasonably fund retirement into their late 80s or beyond. A higher drawdown rate without adjustments shortens that significantly.

Can I access my super at 60?

Yes. Australia’s preservation age is 60 for anyone born after 30 June 1964. You can access your super at 60 if you have met a condition of release, such as retiring or ceasing an employment arrangement. This is separate from the Age Pension, which isn’t available until 67. The Wealthlab Podcast episode Is 61 the New Retirement Age? covers preservation age and conditions of release in plain language.

Will I get the Age Pension with $720K in super?

Possibly not immediately at 67 if your balance is still close to $720K, as that amount may sit above the full pension assets test threshold. However, as your balance draws down through your 60s and 70s, many retirees with similar starting balances transition from no pension, to a part pension, to eventually a fuller entitlement. A lot depends on other assets outside super as well.

Does owning my home affect retirement with $720K?

Significantly. The family home is excluded from the Age Pension assets test. For homeowners, this makes pension eligibility more achievable over time. It also means your day-to-day living costs are materially lower without rent or mortgage payments, which directly improves how far your super stretches.

What’s the difference between the Age Pension age and preservation age?

Preservation age (60 for most Australians) is when you can access your super. Age Pension age (currently 67) is when you can apply for the government’s Age Pension payment. They’re separate, and there’s a 7-year gap between them for anyone retiring at 60.

$720K at 60 gives you real options. The balance is meaningful, and with sound planning around drawdown rate, investment mix and future Age Pension entitlements, a comfortable retirement is within reach for many Australians in this position.

The specifics matter a lot though. Whether you’re single or part of a couple, what you spend, how your super is invested, whether you have other assets, and your health all shape what the picture actually looks like. That’s the kind of thing worth working through with someone who can look at your actual numbers.

Take a look at how Wealthlab approaches retirement planning, or if you’re ready for a real conversation, book a free chat with the team.