$510,000 in super at 60 is a solid starting point. You are above the median Australian super balance for this age group and within reach of ASFA’s comfortable retirement benchmark. The honest question is not whether $510K is enough in principle. It is whether your specific combination of spending expectations, housing situation and investment approach makes it work for the retirement you actually want.

Here is what the numbers show.

Is $510K Enough to Retire at 60 in Australia?

Yes, for most single homeowners with moderate spending expectations. $510K at 60 sits below ASFA’s comfortable retirement benchmark of $630,000 for singles at age 67, but you are retiring seven years earlier. With sensible spending around $45,000 to $50,000 a year, a balanced investment option and the Age Pension supplementing income from 67, it is a workable and genuinely comfortable position.

The three things that determine whether it works:

Home ownership. Without rent or mortgage payments, your required annual income from super is substantially lower. The ASFA comfortable standard for a single homeowner is $54,240 a year (February 2026). For renters it is considerably more. $510K at 60 works comfortably for homeowners and is tighter for renters.

The seven-year gap. You can access your super tax-free from 60, but the Age Pension does not start until 67. At $45,000 annual spending and 5% net returns, you would draw down roughly $210,000 to $220,000 between 60 and 67, arriving at pension age with around $290,000 to $310,000 remaining.

Investment mix. At 60, you likely have 25 to 30 years of retirement ahead. A balanced or growth option, typically 60 to 70% growth assets, keeps your money growing rather than eroding against inflation in a cash account.

What Lifestyle Can $510K Support?

With careful budgeting, retiring at 60 with $510K can still allow for:

- Essential household costs (utilities, food, and insurance)

- Basic healthcare expenses

- Transport or vehicle upkeep

- Modest domestic travel

- Dining out, hobbies, and leisure activities

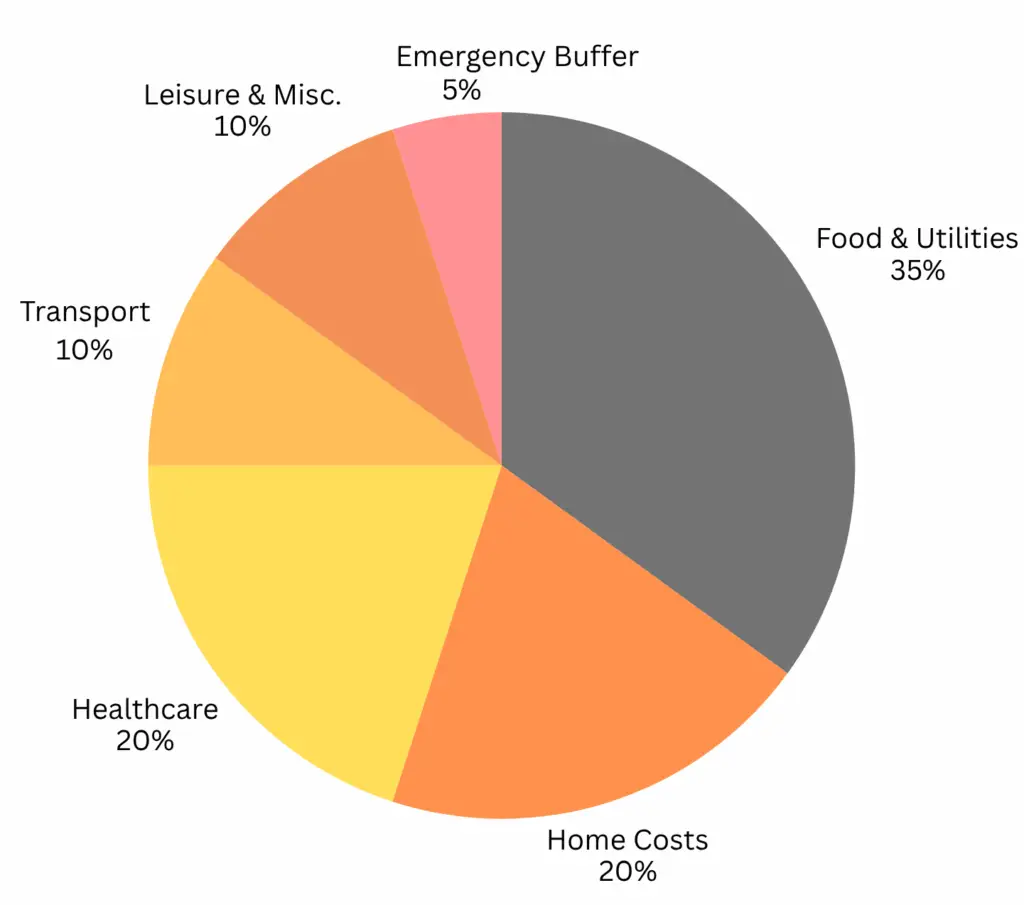

Suggested Budget Breakdown (for $30K/year)

| Category | % of Budget |

|---|---|

| Food & Utilities | 30% |

| Housing Costs | 20% |

| Healthcare | 20% |

| Transport | 10% |

| Leisure & Travel | 15% |

| Contingency/Emergencies | 5% |

How Long Will $510K Last?

Projection assuming 5% net annual return in an account-based pension:

| Annual spending | Super remaining at 67 | Years before balance runs low | With Age Pension top-up |

|---|---|---|---|

| $35,000 | ~$380,000 | ~28 years (to age 88) | Well into 90s |

| $45,000 | ~$310,000 | ~21 years (to age 81) | Mid to late 80s |

| $55,000 | ~$240,000 | ~15 years (to age 75) | Early to mid 80s |

| $65,000 | ~$165,000 | ~11 years (to age 71) | Late 70s |

The Age Pension substantially changes the picture from the late 60s and 70s onwards. A single homeowner qualifies for the full Age Pension once assets fall below roughly $314,000 and a part pension on a taper up to around $695,000. At $45,000 spending from 60, arriving at 67 with about $310,000 puts you close to the full pension threshold. Combined income from super drawdown and pension would sustain a comfortable lifestyle well into your 80s.

Retiring at 55, 60, and 65 with $510K: How the Age Changes Everything

This is one of the most useful comparisons for anyone approaching retirement with this balance, because the age you stop work changes the financial picture dramatically.

Retiring at 55 with $510K

Super cannot be accessed until age 60, so retiring at 55 means five years of living expenses from non-super savings or other income before you can touch your super at all. On $510K in super alone, this is very tight unless you have substantial savings outside super. The seven-year gap before the Age Pension also becomes a twelve-year gap from age 55. Retiring at 55 with $510K is possible with careful planning and outside assets, but it requires a genuine assessment of what you have beyond super.

Retiring at 60 with $510K

This is the ideal entry point. You can access your super tax-free from 60 once you have met a condition of release. The seven-year gap to the Age Pension is manageable at moderate spending levels. At $45,000 annual spending, you arrive at 67 with around $310,000 in super and likely qualify for close to the full Age Pension, giving you a combined annual income of around $45,000 to $55,000 from that point.

Retiring at 65 with $510K

Waiting until 65 means two extra years of growth and contributions (potentially an additional $50,000 to $80,000 in super depending on returns and salary sacrifice), and only two years of self-funding before the Age Pension starts at 67. The financial picture at 65 is considerably more comfortable than at 60. Combined income from super drawdown and near-immediate Age Pension eligibility could support $50,000 to $60,000 a year from 67 with significantly less pressure on the balance. For someone on the fence between 60 and 65, the maths strongly favours working a few more years.

What Lifestyle Does $510K Support?

According to the ASFA Retirement Standard (February 2026 update):

- $35,199 a year for a modest lifestyle (single homeowner)

- $54,240 a year for a comfortable lifestyle (single homeowner)

- $50,866 a year for a modest lifestyle (couple homeowners)

- $77,375 a year for a comfortable lifestyle (couple homeowners)

At $510K with $45,000 annual spending, a single homeowner can live between the ASFA modest and comfortable standards. That means all essentials are covered well, with private health insurance, a reasonable car, regular domestic travel and social spending. Not the full ASFA comfortable standard, but genuinely comfortable for most people.

A sample $45,000 annual budget:

| Category | Annual spend (approx.) |

|---|---|

| Groceries and food | $8,000 |

| Housing costs and rates | $5,000 |

| Healthcare and private health | $7,000 |

| Transport | $4,500 |

| Travel and leisure | $12,000 |

| Clothing and personal | $4,000 |

| Utilities and phone | $4,000 |

| Contingency buffer | $500 |

What Happens at Age 67?

The Age Pension starts at 67 for anyone born on or after 1 January 1957, subject to assets and income tests through Centrelink. The application is not automatic: you need to apply through Services Australia and meet both tests.

At $510K drawing down at $45,000 a year from 60, you would arrive at 67 with approximately $310,000 in super. For a single homeowner, that is close to the full pension threshold of roughly $314,000. You would likely receive close to the full Age Pension rate of approximately $29,754 a year.

Combined with a reduced super drawdown of around $15,000 to $20,000 a year from 67, your total annual income would be roughly $45,000 to $50,000 a year, sustaining your pre-pension lifestyle well into your 80s.

Current 2026 Age Pension rates: approximately $29,754 a year for singles and $44,856 for couples (including supplements).

The Smart Way to Draw Down $510K

Set up an account-based pension. Converting your super to a regular income stream keeps it invested and growing while you draw a tax-free income. It is far more efficient than taking lump sums, which can deplete your balance quickly and disrupt your Centrelink position.

Stay invested for growth. The temptation at 60 is to move everything to cash. This feels safe but loses ground to inflation over a 30-year retirement. In Episode 1 of the Wealthlab Podcast, Scott and Phil ran through a real case study showing that a couple in a conservative portfolio ran out of money 15 years earlier than the same couple in a growth option, on identical spending. The investment mix matters more than most people realise.

Consider part-time work in the early 60s. Even $15,000 to $20,000 a year from casual or part-time work meaningfully reduces how fast you draw down super. One or two days a week for the first three years of retirement can add years to your retirement runway.

Plan the gap years deliberately. The seven years from 60 to 67 are the most financially critical. Overspending in this period, particularly large lump sum withdrawals for renovations or travel, can significantly reduce what you have when the Age Pension arrives. Set a deliberate annual spending target for the gap period.

Watch sequencing risk. A significant market fall in your first two to three years of retirement, when your balance is at its highest and you are drawing regularly, can have an outsized impact on long-term outcomes. Keeping one to two years of spending in cash provides a buffer so you are not forced to sell growth assets at a loss during a downturn.

Key Risks to Watch

Healthcare costs. These increase significantly in later retirement. Building a healthcare buffer from the start, rather than treating it as a future problem, keeps your financial plan intact.

Lifestyle inflation. Early retirement often brings higher spending on travel, experiences and helping family. This is fine in moderation, but every extra $10,000 spent per year reduces your estimated balance at 67 by roughly $70,000 to $80,000 over seven years.

Inflation. A 3% annual inflation rate means your spending needs increase in dollar terms over time. A growth investment option and annual budget reviews address this more effectively than a cash-based strategy.

How Does $510K Compare to Other Balances?

To put your position in context across the series of balances we cover:

- $510K at 60 is workable for a comfortable lifestyle at moderate spending. Slightly below ASFA’s comfortable benchmark. Relies on the Age Pension providing meaningful top-up from 67.

- $570K at 60 gives a bit more breathing room, approaching ASFA’s comfortable standard for singles.

- $610K at 60 is at or above ASFA’s comfortable benchmark, with more flexibility on spending.

If you are weighing up working an extra year or two to boost from $510K to $570K or $610K, the difference is genuinely meaningful in terms of lifestyle flexibility and reduced spending pressure in the pre-pension years.

FAQs: Retiring at 60 with $510K

Can I retire at 60 with $510K in Australia?

Yes, comfortably for a single homeowner spending around $40,000 to $50,000 a year. At $45,000 annual spending with a balanced investment option and Age Pension support from 67, $510K funds a comfortable retirement well into your 80s.

How long will $510K last in retirement at 60?

At $45,000 annual spending and 5% net returns, approximately 21 years from age 60, taking you to around 81. With a near-full Age Pension from 67 as your balance draws down, combined income extends your retirement well into your mid to late 80s.

Can I retire at 55 with $510K?

It is difficult without significant assets outside super. Super cannot be accessed until 60, so you would need five years of income from other savings. The gap to the Age Pension also extends to 12 years rather than seven. It is possible but requires careful assessment of non-super assets and very disciplined spending.

What lifestyle does $510K support at 60?

Between ASFA’s modest and comfortable standards for a single homeowner: all essentials covered, private health insurance, a reasonable car, regular domestic travel, dining out and social spending. Approximately $45,000 a year in a homeowner context.

Will I get the Age Pension with $510K at 60?

Almost certainly by the time you reach 67. At $45,000 annual spending from 60, you would arrive at 67 with roughly $310,000 in super, close to or at the full Age Pension threshold for a single homeowner. The exact amount depends on total assets at 67.

Should I keep working to increase my balance beyond $510K?

The maths supports it, if you can. Working to 62 or 63 could add $60,000 to $100,000 to your balance while also reducing the self-funding gap from seven years to four or five. The difference between $510K and $570K at 60 is meaningful in terms of lifestyle flexibility and reduced annual pressure on your drawdown.

Is $510K above or below average for retirement in Australia?

Above the median. The median super balance for men aged 60 to 64 is around $302,000 and for women around $211,000. $510K puts you significantly above the median for both groups, though below ASFA’s comfortable retirement benchmark of $630,000 for singles at 67.

Ready to work out exactly what $510K means for your retirement? Book a free call with the Wealthlab team and get a retirement income plan built around your specific numbers.