If you are 62 and have around $445,000 in superannuation, you are probably asking yourself: is this enough to retire comfortably, or should I keep working a few more years?

The good news is that yes, you can retire at 62 with $445K. It requires careful planning, realistic expectations, and smart financial choices. While this amount will not cover a luxury retirement, it can absolutely provide a secure, comfortable, and enjoyable lifestyle, especially if you own your home and plan well for the Age Pension that starts at 67.

This guide explains how to make your super last, what lifestyle you can expect, where $445K sits by Australian standards, and the key strategies to make retiring at 62 both practical and fulfilling.

Understanding Retirement at 62 in Australia

Retirement looks different for everyone. Some people want to travel and explore new hobbies, while others simply want to enjoy life without financial pressure. At 62, you have already reached your preservation age, which means you can access your super tax free even though you are not yet eligible for the Age Pension.

That makes ages 62 to 67 a crucial transition period. You will rely primarily on your super drawdowns during this phase. Once you reach 67, the Age Pension can supplement your income and help extend your super further.

Planning how to bridge this five-year gap is one of the most important steps you can take for a financially secure retirement.

Where Does $445K Sit by Australian Standards?

Before running the projections, it is worth knowing where $445,000 actually sits nationally.

ASFA data from the ATO shows the average super balance for the 60 to 64 age group is approximately $430,000 to $450,000 for men and $330,000 to $350,000 for women. At $445,000, you are right at or above the national average for your age group.

ASFA’s February 2026 Retirement Standard sets $630,000 as the comfortable retirement benchmark for a single homeowner at age 67, and $730,000 for a couple. At 62, with five years of drawdowns ahead before reaching that benchmark age, $445K requires discipline to arrive at 67 in good shape. But as the projections below show, it is achievable.

The important context for most Australians is that $445K is not a low balance. Most people in this country retire with less. You are working with a real number.

See how you can retire at 62 with $445K comfortably, wisely, and confidently.

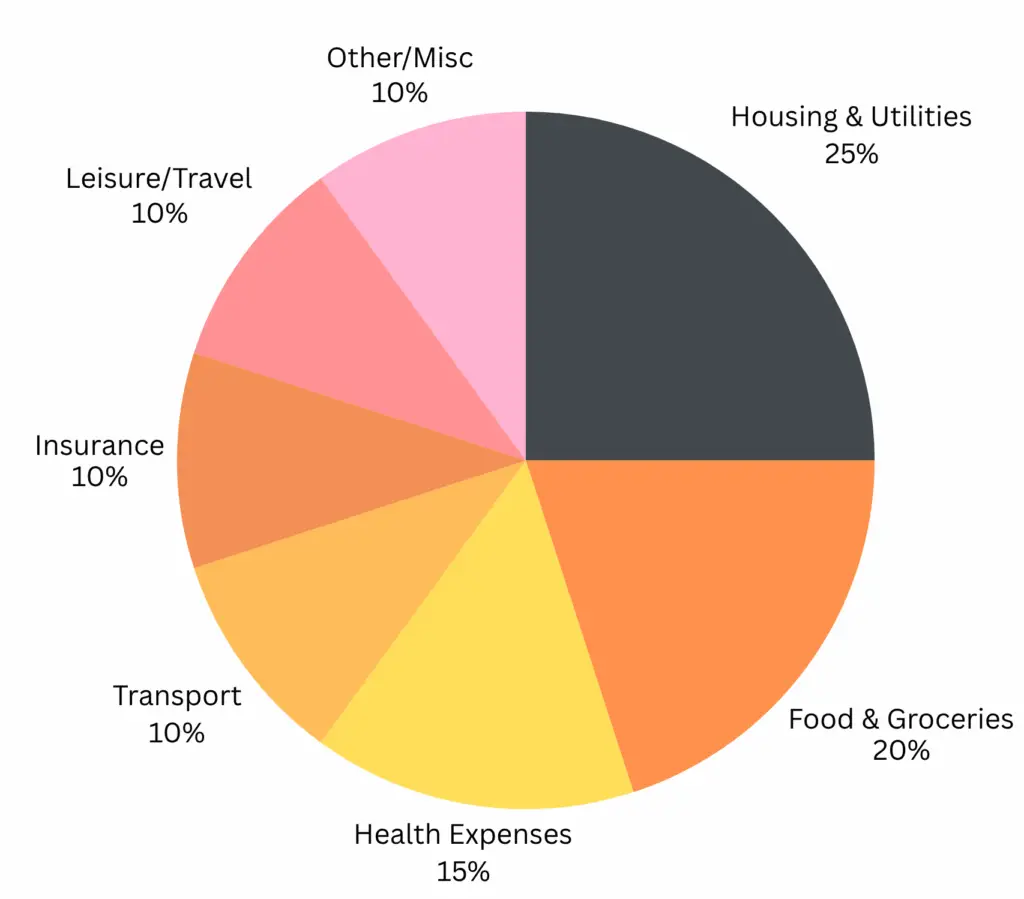

Example: Retiring on a $25K Annual Budget

If you plan to live modestly and budget around $25,000 per year, here’s how your spending might look:

| Category | Estimated % |

|---|---|

| Housing & Utilities | 25% |

| Food & Groceries | 20% |

| Healthcare | 15% |

| Transport | 10% |

| Insurance | 10% |

| Travel & Leisure | 10% |

| Miscellaneous / Buffer | 10% |

This type of lifestyle focuses on essentials while leaving some room for leisure, occasional travel, and small luxuries perfectly achievable for many Australians with $445K in super.

How Long Will $445K Last If I Retire at 62?

The original projections on this page used a 2.5% return assumption. That reflects a cash or very conservative option, not a balanced portfolio. A balanced account-based pension invested in a moderate growth option has historically returned around 5% per annum net of fees. Here are updated projections at three spending levels.

Scenario A: $25,000 per year at 5% return

| Age | Opening balance | Annual drawdown | 5% return | Closing balance |

|---|---|---|---|---|

| 62 | $445,000 | $25,000 | $21,000 | $441,000 |

| 63 | $441,000 | $25,000 | $20,800 | $436,800 |

| 64 | $436,800 | $25,000 | $20,590 | $432,390 |

| 65 | $432,390 | $25,000 | $20,370 | $427,760 |

| 66 | $427,760 | $25,000 | $20,138 | $422,898 |

| Age 67 | $422,898 | Age Pension eligibility |

At $25,000 per year with a 5% return, $445K barely reduces. You arrive at 67 with approximately $423,000, almost the same as you started with.

Scenario B: $35,000 per year at 5% return

| Age | Opening balance | Annual drawdown | 5% return | Closing balance |

|---|---|---|---|---|

| 62 | $445,000 | $35,000 | $20,500 | $430,500 |

| 63 | $430,500 | $35,000 | $19,775 | $415,275 |

| 64 | $415,275 | $35,000 | $19,014 | $399,289 |

| 65 | $399,289 | $35,000 | $18,214 | $382,503 |

| 66 | $382,503 | $35,000 | $17,375 | $364,878 |

| Age 67 | $364,878 | Age Pension eligibility |

At $35,000 per year, you arrive at 67 with approximately $365,000. That is above the full Age Pension threshold for a single homeowner ($314,000) but you will move below it within a few years of continued drawdown, qualifying for increasing pension support.

Scenario C: $45,000 per year at 5% return

| Age | Opening balance | Annual drawdown | 5% return | Closing balance |

|---|---|---|---|---|

| 62 | $445,000 | $45,000 | $20,000 | $420,000 |

| 63 | $420,000 | $45,000 | $18,750 | $393,750 |

| 64 | $393,750 | $45,000 | $17,438 | $366,188 |

| 65 | $366,188 | $45,000 | $16,059 | $337,247 |

| 66 | $337,247 | $45,000 | $14,612 | $306,859 |

| Age 67 | $306,859 | Age Pension eligibility |

At $45,000 per year, you arrive at 67 with approximately $307,000, just below the full Age Pension threshold for a single homeowner. That means the full Age Pension of $31,223 per year starts immediately at 67.

These are estimates based on consistent returns and spending. Actual outcomes vary with investment performance and timing.

What the Age Pension Adds From 67

From 20 March 2026, the full Age Pension rates are:

| Fortnightly | Annual | |

|---|---|---|

| Single (full pension) | $1,200.90 | ~$31,223 |

| Couple combined (full pension) | $1,810.40 | ~$47,070 |

Source: Services Australia: Age Pension rates

Assets test thresholds for homeowners from March 2026:

| Full pension below | Pension cuts out above | |

|---|---|---|

| Single | $314,000 | $695,500 |

| Couple | $470,000 | $1,075,500 |

The Age Pension does not just top up your income. It fundamentally changes how long your remaining super lasts by reducing the amount you need to draw from it each year. By the time you are in your mid 70s, a combination of Age Pension plus a modest super drawdown can comfortably cover the ASFA modest retirement standard ($36,700 per year for a single homeowner).

Many retirees also qualify for the Commonwealth Seniors Health Card from 67, which provides discounts on pharmaceutical costs, utilities, healthcare, and transport. This reduces real living costs well beyond the pension payment itself and is often overlooked in retirement planning.

Scott and Phil walked through exactly how the Age Pension assets test works in real scenarios in Episode 10 of the Wealthlab Podcast: How the Age Pension Really Works With Real Case Studies. Highly recommended if you want to understand how your drawdown timing affects what you receive from Centrelink.

Example: Retiring on a $25,000 Annual Budget

If you plan to live modestly and budget around $25,000 per year, here is what a realistic and sustainable retirement budget might look like for a homeowner:

| Category | Estimated percentage |

|---|---|

| Housing and utilities | 25% |

| Food and groceries | 20% |

| Healthcare | 15% |

| Transport | 10% |

| Insurance | 10% |

| Travel and leisure | 10% |

| Miscellaneous and buffer | 10% |

This lifestyle focuses on essentials while leaving room for leisure, occasional travel, and small luxuries. It is perfectly achievable for many Australians with $445K in super, particularly those who own their home and have no debt.

The Advantage of Homeownership

Owning your home is one of the biggest advantages when retiring early. Without rent or mortgage payments, your fixed expenses drop significantly, meaning more of your super goes toward essentials, healthcare, and leisure rather than housing costs.

Your home is also completely exempt from the Age Pension assets test regardless of its value. A $900,000 family home does not count as a financial asset. Only your super, bank accounts, investments, and other assets are assessed.

If you do not own your home, you still have options. You could downsize and contribute up to $300,000 per person into super through the downsizer contribution, relocate to a more affordable area, or supplement income with light part-time work in the early years. These strategies reduce pressure on your super during the critical 62 to 67 gap.

Making Your Super Last Longer: Five Strategies That Work

Even with a solid balance, smart financial decisions in the years immediately after retirement have an outsized impact on how long your money lasts.

Use an account-based pension from day one. Once you retire, convert your super into an account-based pension. In pension phase, investment earnings are completely tax free (0%), compared to 15% in accumulation phase. On $445,000 earning 5%, that is $22,250 in annual earnings with zero tax instead of $3,338. This difference compounds meaningfully over a 25-year retirement. Set up the pension on the day you retire, not weeks or months later.

Invest in a balanced option, not cash. Too much cash feels safe but loses value against inflation over time. A balanced or moderate growth option has historically returned around 5 to 7% per annum. The difference between a 2.5% return and a 5% return on $445,000 over 20 years is enormous. Hold 12 to 18 months of living expenses in cash as a buffer and keep the remainder invested in a balanced growth option. This is the structure that protects you against short-term volatility while keeping your long-term returns meaningful. Scott covered this directly in Episode 1 of the Wealthlab Podcast.

Delay large withdrawals. Avoid major lump sum withdrawals before the Age Pension starts at 67. Smaller, consistent drawdowns matched to your actual budget extend your super life significantly. Large early withdrawals permanently remove capital that would otherwise compound for decades.

Consider part-time or casual work. Even one or two days of paid work per week can supplement your income, reduce pressure on your super, and boost social engagement. Drawing $10,000 to $15,000 per year from work instead of from super during the 62 to 67 gap preserves tens of thousands in compounding capital.

Check your Age Pension eligibility at 67. Even with meaningful super savings, you may qualify for a partial Age Pension or Commonwealth Seniors Health Card from 67. Apply up to 13 weeks before your 67th birthday. If your claim is processed before your birthday, payments start from the day you turn 67. A late application means a later start date and forfeited pension income.

Retirement Investment Options at 62 and Beyond

If you are 62 or older, your investment approach should balance security and long-term growth. Here are the main structures worth understanding:

Account-based pensions provide flexible regular income, tax free withdrawals after 60, and continued investment growth inside the super system. This is the right structure for most retirees from day one.

Balanced or growth super funds help protect against inflation while generating returns. Most major industry funds offer balanced options with long-term returns of 6 to 8% per annum, well above cash rates.

Dividend-paying ETFs or shares held outside super can provide reliable income with long-term capital growth if you have savings beyond your super balance. Fully franked dividends from Australian companies are particularly tax efficient for retirees, since franking credits can be refunded in full when your overall tax rate is low or zero.

Term deposits and bonds provide low risk income suitable for your short-term cash buffer. At current 2026 rates of around 4 to 5%, term deposits are a reasonable option for 12 to 18 months of living expenses.

A diversified structure combining these elements gives your retirement savings both stability and long-term growth. For more on how to structure your investment portfolio in retirement, see our guide on should I keep investing after retirement?

Retiring at 62: Smart Planning Tips

If you are thinking of retiring at 62 with $445K, here are the practical steps to follow:

Review your spending and lifestyle expectations before you stop working. Build a realistic monthly budget based on your actual costs, not estimates.

Keep one to two years of living expenses in cash at all times for emergencies and short-term stability. This is your buffer that allows your growth investments to compound without being forced to sell at a bad time.

Consider transitioning into retirement gradually through part-time or casual work in your first year or two, rather than stopping completely. This significantly reduces early drawdown pressure and keeps more capital working.

Review your super fund’s performance and fees at least every two years. Even a 0.5% difference in annual fees on $445,000 costs $2,225 per year, compounding over time into a meaningful difference by retirement.

Seek advice from a qualified financial planner to optimise your super structure, minimise tax, and maximise Age Pension eligibility. The decisions made in the first two years of retirement often have the largest long-term impact.

Want to see how different spending levels affect how long your $445K lasts? Use the Wealthlab super calculator to model your specific scenario in a couple of minutes.

FAQs: Retiring at 62 in Australia With $445K

Can I retire at 62 with $445K in super? Yes. At $25,000 per year with a 5% investment return, your balance barely moves over the 62 to 67 gap and you arrive at 67 with approximately $423,000. At $35,000 per year you arrive with around $365,000. At $45,000 per year you arrive with approximately $307,000 and qualify for the full Age Pension immediately at 67. In all three scenarios, the Age Pension provides a meaningful income supplement from 67 onwards.

What is the retirement savings benchmark for age 62 in Australia? The ASFA Retirement Standard (February 2026) sets $630,000 as the comfortable retirement benchmark for a single homeowner at age 67 and $730,000 for a couple. At $445K retiring five years earlier at 62, you are below the benchmark but with disciplined spending of $25,000 to $35,000 per year, your balance tracks close to these figures by the time you reach 67.

How long will $445K last if I retire at 62? At $25,000 per year with a 5% return, $445K effectively holds its value over the 62 to 67 gap. From 67, the Age Pension supplements your income, reducing the annual drawdown needed and extending the life of your remaining balance well into your 80s and beyond. At higher spending levels of $35,000 to $45,000 per year, you arrive at 67 with $307,000 to $365,000 remaining and qualify for increasing Age Pension support as the balance continues to reduce.

Will I get the Age Pension at 67 with $445K at 62? It depends on your drawdown rate. If you spend $25,000 per year, you arrive at 67 with approximately $423,000, which is above the full pension threshold ($314,000 for a single homeowner). You will receive a part pension that grows as your balance reduces. If you spend $45,000 per year, you arrive at 67 with approximately $307,000, just below the threshold, and qualify for the full pension from day one at 67.

What is the Age Pension from March 2026? From 20 March 2026, the full Age Pension pays $1,200.90 per fortnight ($31,223 per year) for singles and $1,810.40 per fortnight ($47,070 per year) for couples combined. Source: Services Australia.

What if I am retiring as a couple with $445K combined? With $445,000 combined, say $222,500 each, the 62 to 67 gap requires careful management on joint spending of $35,000 to $40,000 per year. The couple’s Age Pension from 67 ($47,070 per year combined) provides a strong income floor. For homeowning couples, this combined income supports a comfortable lifestyle in later retirement even after super reduces. Our guide on can couples combine super in Australia covers how to plan two super accounts together.

62 years old retirement: how do other Australians manage? Most Australians retire between 63 and 65, making 62 slightly early but very common. The average retirement age for men is around 64.8 years and for women around 63.3 years according to ABS data. Many who retire at 62 combine super income with light part-time work in their early 60s before fully transitioning to super plus Age Pension income from 67. This hybrid approach is one of the most financially effective ways to retire early in Australia.

Retiring at 62 in Australia with $445,000 in super is genuinely achievable. The plan is straightforward: convert to an account-based pension, invest in a balanced option with a cash buffer, draw at a sustainable rate matched to your actual expenses, and plan your Age Pension claim well before you turn 67. The Age Pension from 67 is not a safety net of last resort. It is a central pillar of a well-structured retirement income plan.

At Wealthlab, we help Australians turn their super savings into lifelong income plans that provide peace of mind and financial independence. Book your free retirement planning session today and start your journey toward a confident and comfortable retirement.